Existing insurers and disruptors are utilizing Artificial Intelligence to create new business models

We can see that Artificial Intelligence (AI) is transforming many parts of our lives, but do we know where this journey is taking us? Insurers need some certainty on what their future will looks like. Some new insurers are trying new business models enthusiastically and then changing direction sharply, like a speedboat swerving to avoid a collision. The larger insurers, however, are like large cruise ships; they need to be able to see far ahead before they plot their course, and they don’t want to keep changing direction.

This research tried to identify the viable AI driven business models to help give some clarity. Some traditional insurers are just trying to be more effective with AI, while others reinvent themselves to fully utilize the new capabilities available. Tech-savvy companies from outside the sector like Tesla, are entering and disrupting it. Would these diverging paths continue, or would they converge in the future towards one, ideal, business model? This research focused on one example of a traditional insurer and one new tech-savvy disruptor and evaluated whether their models are converging.

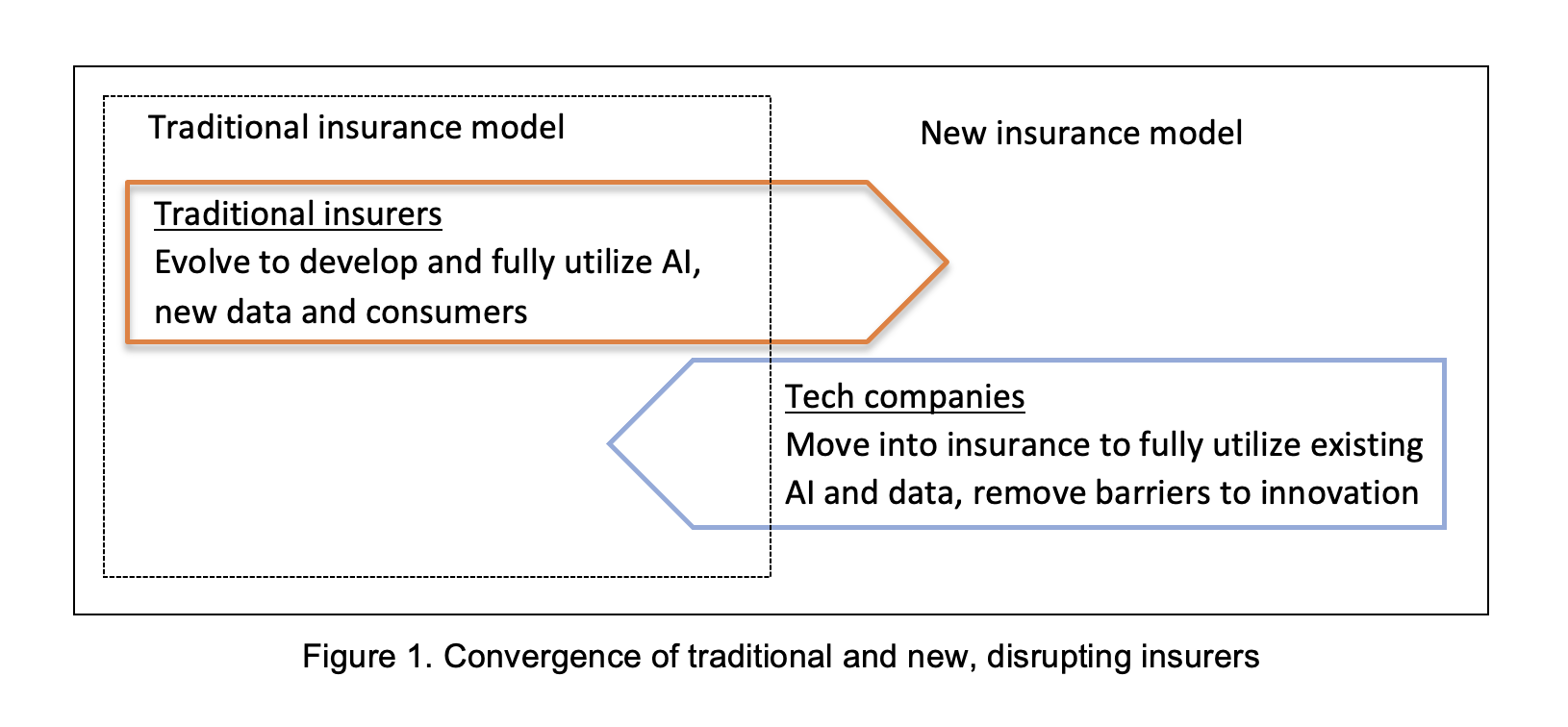

AI is changing the insurance value chain, as illustrated in figure 1. Most new insurers, like Tesla, offer fully automated simple services. The traditional insurers offer some of their simpler services in this way. The more complex services are supported with AI, but a human makes the final decision. An example of this are audits for fraud, where the AI identifies unusual patters and cases for an expert to evaluate.

There are signs of convergence between the models of traditional and new insurers. First, there is convergence in technologies, such as the use of chatbots utilizing AI. Second, there is a convergence in processes, for example, the interaction with the consumer. Third, there is convergence in the strategy on costs and pricing.

However, there are two areas where there seems to be a limit on convergence, which seems to suggest the business models of the incumbent and the disruptor will remain distinct. These are: (1) evaluating risk and (2) the cost of attracting the user and profitability.

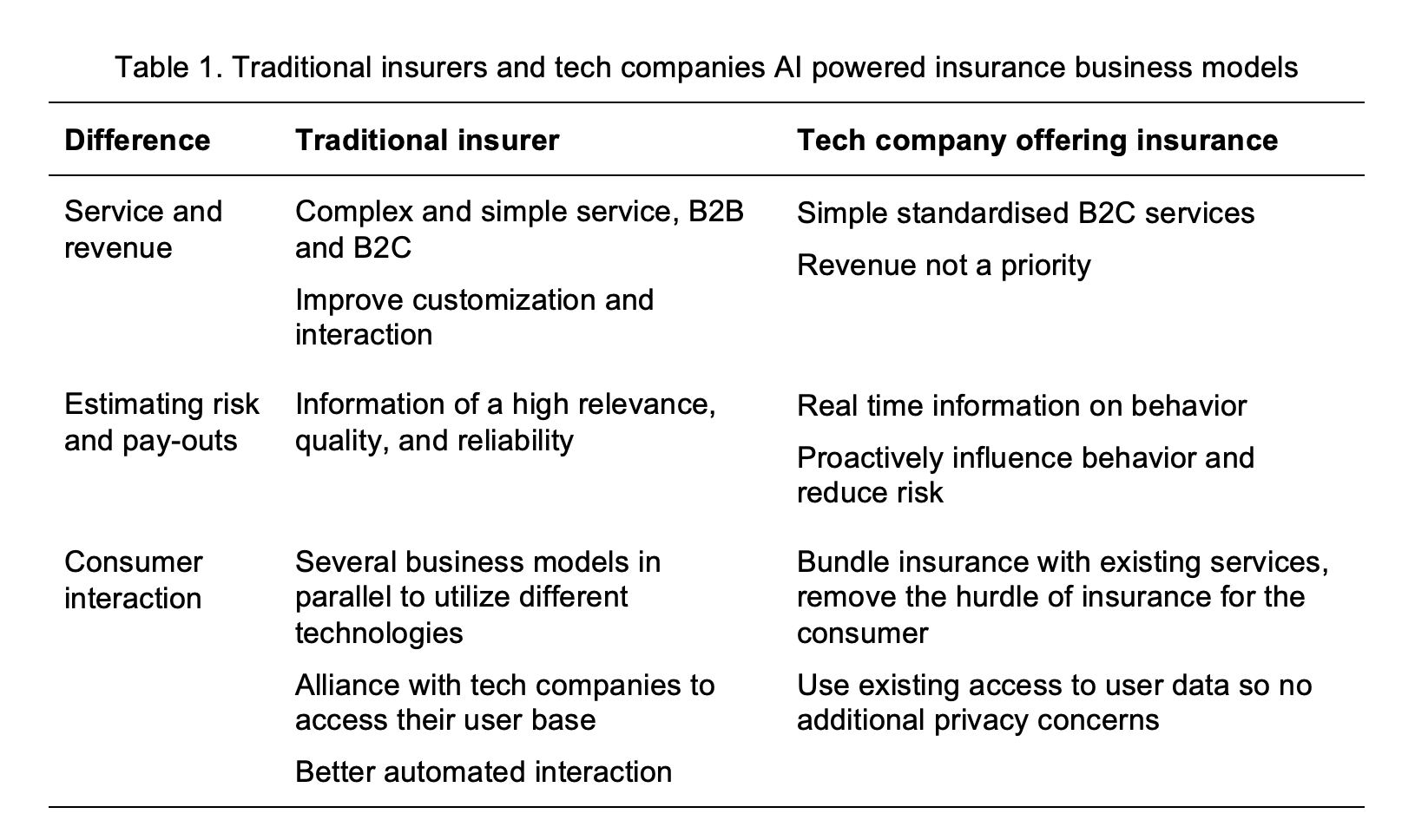

Despite some convergence, certain differences are likely to remain even after this transitionary period. This is because the two models have distinct competitive advantages. Traditional insurers no longer monopolize the capability of providing insurance, but they still have the existing user base and utilize it to evaluate risk. Technology-savvy companies that now offer insurance, have their own forms of engagement with their consumers, use different methods to evaluate risk due to their access to real time data, and do not prioritize generating revenue but instead utilize insurance to increase their user base, overcome barriers, and reduce the overall cost of their products and services.

Therefore, when insurers are thinking about how to utilize AI and plot their course through the turbulent, unpredictable times ahead, they should stay true to what they are. This is their comparative advantage.

Dr Alex Zarifis is a lecturer at the University of Nicosia in Cyprus.

This article is adapted from his paper, “Evaluating the New AI and Data Driven Insurance Business Models for Incumbents and Disruptors: Is there Convergence?” available from https://doi.org/10.52825/bis.v1i.58.

What is on this page:

Related content

Why Community Financial Institutions Need an AI Operating System

I went to a Digital Banking conference and an AI event broke out!