In-depth fintech research and analysis with specialist MSc students

Article written by Ksenia Siedlecka, Financial Services and Fintech Sector Engagement Manager at Edinburgh Innovation

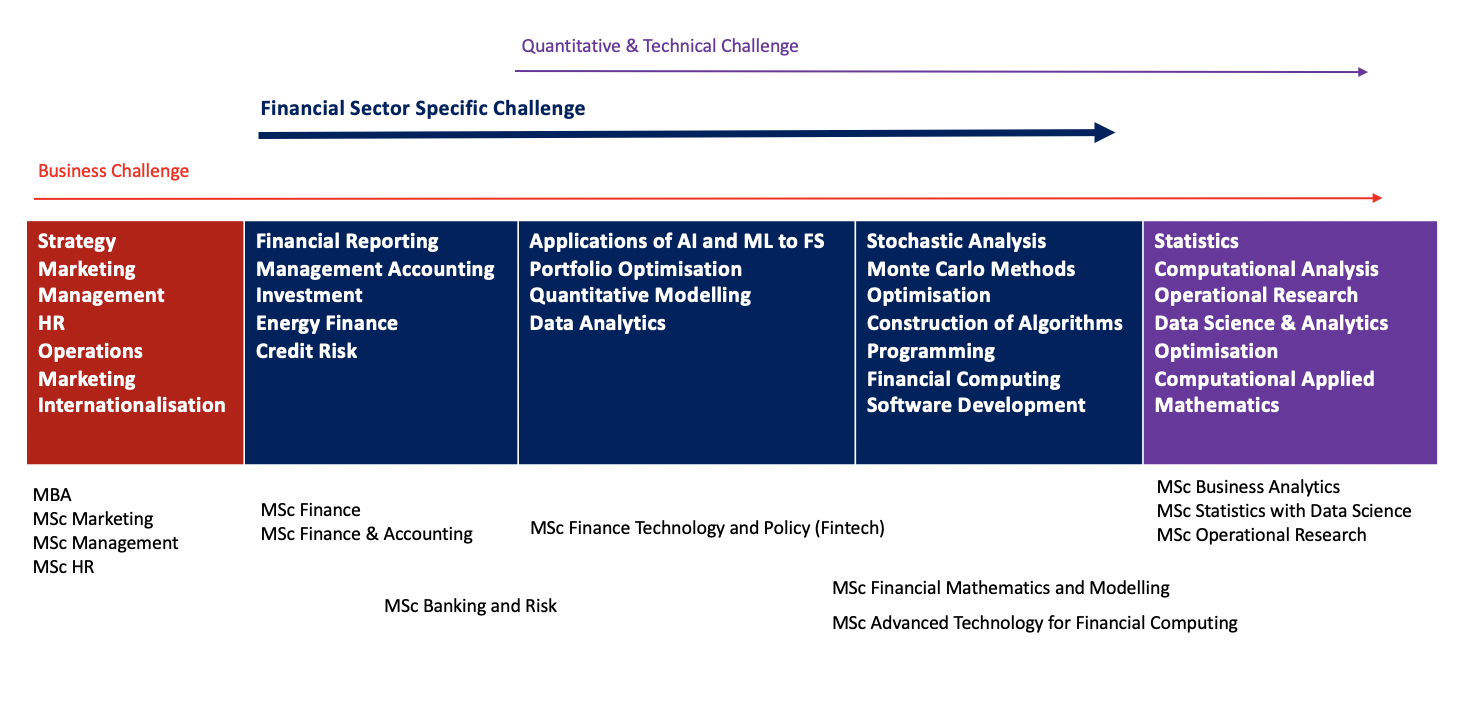

We are currently looking for projects for a variety of MSc programmes with finance and fintech focus (MSc Fintech ”“ Finance, Technology, Policy, MSc Banking and Risk, and MSc Finance, MSc Financial Mathematics). We also have a number of business and data science MSc programmes which are popular with Financial Services and Fintech companies looking to propose projects (e.g. Business Administration, Business Analytics, Statistics). With such a fantastic selection of programmes, we are able to tackle a variety of business challenges. Our students are among the best in their field and combine their specialist subject knowledge and management skills with the refinement offered through our 12-month, intensive programmes. Projects are delivered free of charge and supported by our world-leading academics at The University of Edinburgh. We offer different types of projects and will match you with an individual postgraduate student with the specialised skill set suited to your business challenge and research needs.

Our Business School students can help tackle questions related to corporate strategy, marketing, finance, internationalisation, product development, HR, operations management, change management and many others. The MSc in Finance programme covers all aspects of investment, corporate and energy finance. MSc Accounting and Finance could help with topics on financial reporting and management accounting. MSc Banking & Risk projects could cover such topics as analysis of corporate financial information, credit risk management, econometrics applications and many others. We can consider almost any topic that has a finance, accounting, investment, energy market, banking or risk focus. Successful projects tend to have an empirical element, which has practical relevance. Our students are keen to work with practitioners on projects which will be of real value to them, helping them find solutions to strategic financial issues such as validity forecasting, forecast asset market returns, risk modelling, dynamic lifecycle strategies etc.

MSc Financial Mathematics students will work on a real mathematical finance problem and can utilize specialist techniques such as stochastic analysis, Monte Carlo methods, statistics and optimisation, construction of algorithms and programming skills. Projects often require the design and implementation of computational analysis to a specific area, and can involve the application and implementation of existing mathematical models, or development of new approaches to solution methods. Quantitative modeling, data analytics, financial computing and software development projects can be tackled by our computer science students from MSc Advanced Technology for Financial Computing.

The MSc Finance, Technology and Policy (Fintech) prepares students with technical skills and knowledge of programming, artificial intelligence and machine learning who also understand financial markets and regulations so they are ready to develop technological solutions fit for the financial sector. We are particularly interested in dissertation topics in applications of artificial intelligence and machine learning, data analytics, and portfolio optimisation. Example topics include: building robo-advise algorithms using ML; pattern recognition in big data (including alternative data) using ML; optimal execution strategy with particular emphasis on trading securities in ratio, and many others. Can you help?

If so, we’re looking for companies to submit project ideas by approx. 25 January 2021. In return, you’ll benefit from the insight of one of our high-calibre postgraduate students, including a substantial report featuring extensive research, rigorous analysis and practical conclusions.

To discuss further, contact Ksenia Siedlecka, Financial Services and Fintech Sector Engagement Manager, ksenia.siedlecka@ei.ed.ac.uk

Inclusion, fintech and future talent

Inclusion drives fintech innovation

This has been an action-packed time for everyone involved in the FinTech Scotland Cluster. With COVID-19 continuing to have an impact on our lives both at work and at home the energy across the cluster continues to inspire us.

In particular there has been an even stronger focus on inclusion. Since I’ve known it, this topic has always been front of mind for all involved in the FinTech Scotland Cluster. The work over the recent weeks has continued to demonstrate the drive to build an inclusive environment that enables diversity to win, innovative environments to advance future opportunities for all and build business success.

Inclusion driving future talent

We’re continuing to learn about the full range of organisations across Scotland that are working in practical ways to build skills, experience and communities to help people from different backgrounds explore opportunities in FinTech and Tech. It’s always a pleasure to learn about the practical approaches being taken to support and enable inclusion.

Code your Future is strengthening its focus in Scotland. It works with people who have had limited access to education, offering practical tech training to anyone that’s experience problems in getting meaningful work. There are ten graduates on course to graduate in November, who will be looking for opportunities. Previous graduates are working at BBC Scotland and STV, and code your future has plans to support another class of 30 students next year.

We’ve also been working directly with the team Inlcusion Scotland over the past few weeks as we look to expand the FinTech Scotland team through an internship. Inclusion Scotland work to ensure the full inclusion of disabled people into all aspects of Scottish society can be achieved. All of us a FinTech Scotland very much looking forward to adding to the team.

Inclusion drives business development

It’s been great to see the hard work from the team Lloyds Banking Group pay off so successfully as they launched the Launch innovation lab. The innovation themes of digital services and ESG are another example of the conscious focus being given to the topic of inclusion. Congratulations to Inbest and Legado who are both participating in the programme.

Obashi also shared an exciting development this week as it joins the World Economic Forum’s innovators community. An inclusive first for this forum, for Obashi and for Scotland. Obashi’s work is another great example of inclusion driving business development, moving from the oil industry to share its experiences of dataflow frameworks to bring clarity to new sector.

Inclusion drives financial inclusion

Over the last few weeks we have continued to see the efforts of many across the FinTech Scotland Cluster continue their unwavering focus on financial inclusion.

Amiqus continues its work with proxy address and launched a new trial to test the proposition. It works to provide those in danger of losing their home and subsequently their address with a proxy address and the innovation has the potential to ensure people continue to get access to vital services including access to the benefits they need.

FinTech focus on financial inclusion has also been supporting the UK’s Money and Pension Service (MAPS) who has recently launched a UK Financial Wellbeing Strategy. Thank you to, Nude Visible Capital Soar Directid FastPAYE and Money Dashboard for sharing your views. We know there will be more on this over 2021 and that COVID-19 has brought the topic of financial inclusion into sharper view.

Pinsent Masons recent research on Creating a Culture of Support in Financial Services has focused on the topic of Money and Mental health. It draws on a range of perspectives from a wide and diverse group of industry participants and explores a range of initiatives being built to offer inclusive support for those that want it.

And on a final related note, this week has been Talk Money week, another initiative to encourage people to engage in money and to get us all talking about it. Experience shows that money continues to be a taboo subject and research has highlighted that often people find the subject to daunting and complex. FinTech’s such as Sonik pocket and Moneymatix are working to help children engage with money and financial decisions at an early age. A bit like those why’ questions our children are so good at asking, innovations like this might go some way to helping us all talk about money.

Hoping you all stay safe and well.

Nicola

How Fintech is Disrupting Customer Service

Technology has changed our way of life so rapidly that it’s hard to even call them “disruptions” any more. Indeed, today’s technological innovations are all about looking at our current way of life and seeing how else to improve it. This also means that technological innovations will play a big role in shaping our way of life post-COVID.

In particular, the World Economic Forum notes that fintech will play a key role in helping businesses recover from the effects of the pandemic. And while fintech’s role in helping businesses raise capital or invest their funds is clear, there’s also another key way that fintech can help accelerate business processes.

Fintech and customer service

Customer service is one of the biggest pillars of any business operation, and this holds especially true in today’s increasingly connected society. The average consumer is more discerning than ever, and it only takes one bad Tweet or Facebook post for word to quickly get out about your company.

As such, ramping up customer service practices will play a key role in ensuring that these goals are met. Digital adoption is already strong thanks to fintech innovations such as e-wallets and mobile investment apps, but customers still need to know how to properly manage their money. Providing accessible customer service options will therefore become a true marker for whether a bank is ready to succeed in 2021 and beyond.

How Fintech is Disrupting Customer Service in Different Industries

Banking

The Telegraph has recently called for an overhaul of the traditional banking business model in order to address rapidly shifting customer changes, particularly when it comes to value creation amongst consumers. This process can start by offering in-chat services within mobile applications; as it stands, many banking applications still rely on uploading phone numbers and emails onto their applications should customers need more assistance. Adopting in-app chats speeds this process up, but it also means that fintech companies themselves will have to adopt unified data systems that allow agents to get the information they need within a few clicks.

Supply chain

The speed information is shared is now the foundation of a successful supply chain. A post on staying productive in the new normal by Verizon Connect states that fast information sharing is a marker to customers that your business is constantly improving its services to meet their demands. The site also notes that the faster information is shared the more agile a company can be in responding to a customer’s needs. This allows companies on the supply chain to serve more customers faster. Logistics companies who rely on GPS tracking and management systems to give timely parcel updates are but one example of how this speedy information improves customer service.

Retail

Our previous post entitled ‘Card Issuing and Management: Staying Relevant Facing Ever Faster Changing Customer Expectations‘ shows that fintech companies have a huge role to play in paving the way for a stronger retail industry in the aftermath of Covid-19. Card issuing solutions are in line with the rise of alternative payments, whether through digital platforms or via online currencies. These developments prove that access to varied payment channels plays a big role in improving a business’ overall customer service.

Fintech disruptions are part and parcel of our new normal. Indeed, the impact of fintech on customer service across several industries proves just how pivotal these disruptions are when it comes to streamlining business operations while still keeping customers in the loop. Businesses are now looking to plan for post-pandemic business growth, and it looks like fintech solutions will be an essential tool to meet these goals.

FinTech and Translation Industries; Interesting Bedfellows

When one looks at the business challenges and technological advancements, shared by both FinTech and Translation Industries, alike, quite a few interesting synergies emerge, including:

- Both being enablers of global online client interactions

- Both enjoying unlimited client reach

- Both disrupting traditional workflows, via technological advancement

- Shared concerns regarding data security

Enablers

FinTech is one of the most rapidly expanding sectors in the world, revolutionising personal & business finance, via online banking and applications. FinTech has changed the finance game, forever, and has rendered traditional banking methods, extinct.

Whether it is, the exchange of foreign currency, the ability to trade in cryptocurrency, the ease of access to the world of investment, or making payments via mobile, the sheer scale of opportunity is remarkable.

The translation industry, of course, performs the translation & localisation of banking apps, websites, and communications that all enable global trade. New advances & developments in translation technology, have played their part in changing the entire client experience. This could be through automated translation as opposed to human translations, secure portals for the transfer of client files, API technology to connect client and supplier systems, or Online Editor facilities.

Unlimited Client and Workforce Reach

Online workflows & operations mean that, in both industries, there are no geographical barriers to having a global workforce or client base. Translation & localisation also ensure no limitations in the launching of new products to international audiences.

Accredited translation agencies have invested and incorporated the latest technologies within their workflows. Their skillset in managing complex localisation projects, ensures that the FinTech industry can quickly & effectively market their services globally.

Although FinTech communications can be handled seamlessly, accreditation is an altogether different story. One principal issue that FinTech faces when expanding, is navigating the relevant local regulation. With codices differing between, and even within, countries, the legal side of FinTech growth is far from simple.

Technology: Disrupting Traditional Ways of Working

FinTech and Translation companies can successfully operate without necessarily needing brick & mortar facilities. Of course, there are both advantages & disadvantages to fully-online-based organisations; for those with global operations, however, the advantages are manifold. For example, lower operational costs allow SMEs and Start-Ups to invest in personnel and the business itself, rather than being burdened with the heavy cost of facilities.

Although, being location-independent does present its own set of challenges. The puzzles of how to best: manage, motivate, or support staff effectively, for instance.

Data Security

Data security is essential in all industries and sectors; this is especially acute with respect to financial transactions and the security of client translation documents. Unfortunately, we are all too frequently confronted with news of ransomware cyber-attacks, against companies such as North Hydro and Travelex. That said, this threat is perennial to all industries and companies.

Most translation agencies enable clients to order & transfer files online, via a secure Client Portal’. For the most technologically advanced translation companies, the client files are not issued directly to external translators, as was done in the past.

This new workflow facilitates the translation of files directly within the online translation platform, accessed via the unique & secure portal. Maximum security for client IP, is thus, guaranteed.

A Conclusion

As little as five years ago, it was unimaginable to foresee such a rapid shift to mobile apps & online-only operations; it is fascinating to contemplate where we will be in five years’ time.

These technological developments are not only advancing services & capabilities within the industries themselves, but also other, more indirect, business benefits. These include: a global unlimited client base; online-only operations; physical office facilities becoming no longer necessary; or flexible working options.

All of this significantly lowers the barriers to entry for entrepreneurs in all industries internationally. It will be enthralling to see this continued evolution, and what lies ahead for all of us.

This blog was written by Fiona Feldermann McCrae, Managing Partner, at McFelder Translations.

McFelder Translations, an ISO accredited powerhouse with almost two decades of technical experience, is your passport to building a global brand.

If you’d like to find out more about localising your FinTech communications, email: fiona@mcfelder.com.

Website

LinkedIn

Twitter

Instagram

Image created using Canva

GLEIF and Open Future World Directory to enter partnership

The Global Legal Entity Identifier Foundation (GLEIF) and Open Future World have announced a new collaboration to help open finance organisations to work together.

This comes after the launch of the Open Future World Directory , the open finance organisation directory. Thank soo the addition of the Legal Entity Identifiers (LEIs) within the directory, it will be easier to identify who to connect to and do business with.

“The Legal Entity Identifier is a global standard for transparent and unique identification of legal entities. Users of the Open Future World Directory now benefit from quick and easy identification of the listed organization by linking to its validated and verified profile in the Global LEI Repository,”

Clare Rowley, GLEIF Head of Business Operations

“Whether you are talking about customers choosing to share their financial data, or financial institutions and fintechs working together, trust is a key theme in open banking and open finance. LEIs help enhance transparency by making it easier to know who you are dealing with.”

Nick Cabrera, Open Future World co-founder

Small business resilience and the evolution of ecommerce

The continuing shuttering of small businesses on high streets across the country is being accompanied by an unseen birth of new, exciting digital-only small businesses.

Periods of economic downturn typically result in a decline in new business registrations and at the beginning of the pandemic, it looked like UK SMBs were set to follow in this trend. For instance, statistics released by the ONS revealed that business creations slowed during April and May.

Despite this, Companies House figures reveal an overall increase in the number of new company incorporations in Q2 when compared to the previous year. This is indicative of a plethora of new business ventures inspired by our changing way of life.

Many of these emerging businesses are digital-first by necessity of the global lockdown they were born out of. Take for instance an independent hardware store which was already struggling prior to the pandemic. They may now find themselves in a position of renewed success, selling specific gardening tools via Shopify and Instagram marketing. While they may not have a strong credit history they do have a vast data footprint, owing to the numerous systems they rely on to run their business. Each data source, from their accounting package to their POS or ecommerce system provides a valuable yet siloed view of performance.

The shifting value exchange

However, the modern SMB expects systems and services to work together seamlessly and appears more willing to share their data in an open and automated fashion in order to ensure this. For instance, in September of this year, it was reported that the use of open banking had doubled in just nine months – an increase of one million users since January.

This increased appetite for interconnectivity between financial systems has opened the door to a much more collaborative, bespoke and diverse service between small businesses and their financial service providers. This is evidenced by the growing convergence of the POS, ecommerce and lending industries. Square Capital, Shopify Capital and Worldpay Working Capital are just some examples of funding facilities utilising transactional data to determine creditworthiness and offering finance at the point of need for small businesses.

Moving forward, customers who are willing to share their financial data digitally via accounting, ecommerce & POS package authorisation or open banking will likely benefit from a better service and more affordable products. For instance, lenders will be able to offer more favourable rates due to their enhanced ability to calculate risk and the notable reduction in the cost of serving these customers. The end result will be a shifting value exchange for small businesses whereby the benefits of sharing their data will become even more tangible than ever before.

The rise of ecommerce

The conditions of the global lockdown required existing businesses to pivot in order to remain viable. As a result, the period between April and July saw 85,000 UK businesses launch online stores or join online marketplaces. Many of these SMBs thrived during the pandemic as their adoption of ecommerce solutions coincided with a rapid increase in online sales, accelerating e-commerce growth by five years.

With the pandemic shifting the primary channel of trade online, gaining access to ecommerce and point of sale data is now crucial for financial service providers. The mutual benefits of doing so are multifaceted. For instance, commerce data can be used by lenders in particular to improve underwriting processes and credit decisioning. Small businesses will therefore benefit from a faster and fairer service which goes beyond traditional methods of credit scoring to consider their performance from multiple data sources in real-time.

This cultural shift towards enhanced digitisation and the growing importance of ecommerce will likely have a lasting impact on the way we think about the financial health of small businesses. In order to take advantage of this opportunity, financial service providers will need to replace siloed data with a connected ecosystem of unified financial data sources.

This article was written by Pete Lord, CEO and Co-Founder at Codat. Codat lets banks and fintechs plug into their small businesses and the software they use, giving them seamless access to real time customer data. Codat is building an ecosystem of connected datasets that handle the heavy lifting of integrations, leaving providers free to focus on improving their offerings for small businesses.

Photo by BedBible

Calling all Internal Auditors working in the Fintech environment

Calling all Internal Auditors working in the Fintech environment”¦”¦.

For those that don’t know me, please allow me the opportunity to introduce myself. I have worked in and around Internal Audit for more years than I care to admit and have recently started a new adventure as Head of Internal Audit for Modulr Finance based in Edinburgh.![]()

Having moved into a fintech organisation I find myself wondering: “how can I adapt, evolve and innovate the approach to fintech Audit to best meet (perhaps exceed?) the needs of a relatively new and growing fintech industry”?

Over my years of experience, I have (too often) been faced with the negative stigma which can come with our profession. On hearing the words Internal Audit, stakeholders can automatically jump to the old stereotyped assumptions assuming that we prevent innovation and entrepreneurial spirit and struggle to respond to the changes required in such a dynamic and fast evolving industry. Like many of my colleagues and peers, I am committed to banishing this perception and ensuring that the profession continues to build on and evolve approaches which remain robust and sustainable, but can keep pace with and best add value in such a newly evolving, fast paced, dynamic and exciting sector.

How can we make sure we (as a profession) move with the times displaying the agility, flexibility and creativeness required to satisfy the appetite of such a new industry and its many stakeholders? It can be a daunting thought, and one I am sure I’m not alone with!

My belief is that Internal Auditors in fintech have a unique opportunity to help shape the future of fintech, but to do so require a tailored combination of business audit, IT Audit, project management skills blended, a good dose of commercial judgement together with refined and tailored approaches to realise this. Part of the key to our success is collaboration, and with this in mind, I take much pleasure in announcing a collaboration between FinTech Scotland, and the IIA: The FinTech Audit Forum – intended to allow those working within Internal Audit in the Fintech industry to network, share ideas, discus hot topic and tailor their approach.

If you work in fintech, either in Internal Audit, or have a vested interest in this initiative and would benefit from:

- knowledge sharing and asking questions with peers

- hearing shared experiences, views, and responses

- industry insight

- Audit Committee perspectives

- A network of Internal Auditors working within fintech

- Discussion and debate of current/ emerging issues, hot topics, obstacles, changes, regulation etc

- Hearing of proposed/bespoke approaches aimed at the FinTech Internal Audit community and stakeholders

then please let me know and I would be delighted to include you in the FinTech Audit Forum. Our first meeting is on Wednesday 28th of October between 2pm and 3pm. This will be a vitual meeting and we’ll be delighted to see you there.

Photo by bongkarn thanyakij from Pexels

Scotland is Tomorrow: Developing Responsible Investing in Scotland with rTech?

Scottish Fintech has been a key highlight of Scotland’s modern economic rotation. A more sustainable, inclusive and progressive ecosystem. It is helping to change the shape and face of Scottish e-commerce and finance but has it always been changing it to be more responsible?

Despite the COVID-19 lockdown, the delayed COP26 presents a unique opportunity to reinforce Scotland’s position as a global centre for responsible investing. In doing so Scotland competes with every other country to drive leadership and achieve United Nation Sustainable Development Goals (SDGs). Like Scottish Fintech and the formation of the Scottish National Investment Bank, developing and growing Scotland’s responsible investing landscape is a powerful way to move Scotland’s economy to something more purposeful. The key is collaboration, which stimulates innovation, which encourages inward investment, which produces change in Scotland and overseas.

May 2020 saw the launch of Ethical Finance Hub’s new report, Mapping the Responsible Investing Landscape in Scotland’, which examines the responsible investment market in Scotland, looking at:

- History: the history of responsible investing with a focus on Scotland;

- Ecosystem: the composition of the Scottish responsible investment market, and the linkages between different participants;

- Taxonomy: the terms used by Scottish fund managers to describe their approaches to responsible investment; and

- Market Size: The size of the responsible investing market in Scotland, and how it compares to Ireland and the rest of the UK.

The motivation behind the report was to raise awareness and support the growth of the responsible investing market in Scotland. Having engaged with a number of stakeholders, as well as undertaken internal desk-based research, it was apparent that, whilst data on the sector exists for the UK as a whole, there was little or nothing specific to Scotland available. A link to the report can be found here: https://www.ethicalfinancehub.org/investingscotland2020/.

The report sets out the following call to action:

“Across the globe individuals, organisations and governments are starting to move from talk to collective action as we strive to achieve inclusive economic growth without depleting natural resources. It is now widely recognised that the financial services sector has a fundamental role to play in delivering universally supported targets such as the Paris Agreement and the SDGs. However, despite its potential, the current financial system can be a cause of, rather than a solution to, some of the pressing challenges our planet and its people currently face. In trying to address this predicament Scotland is reflecting on its heritage and seeking to emerge as a leading centre for a new financial paradigm that looks beyond profit and shareholder value to deliver social, economic or environmental impact as well as financial returns.”

In parallel Scottish Fintech can now boast over 120 Fintechs, connected with 15 universities, 16 tech spaces, accelerators and incubators. The conditions are fertile for cross pollination between responsible investing initiatives and Fintech. Yet Scottish Fintech and Scottish Asset Management are, at best, acquaintances rather than partners driving true innovation in responsible investment. Only by linking the success and innovation of Scottish Fintech with the opportunity in responsible investing can Scotland truly compete and succeed as a global leader. Bluntly put, Scottish asset managers and asset owners are missing a step in utilising the talent within Scottish Fintech.

Indeed a key observation in the report was the lack of collaboration between Scottish Fintech and Scottish asset managers in creating new solutions to expand investment, improve data and clarify the taxonomy (the universe of terminology). This is totally in keeping with what I set out as a New Fund Order’, the enablement and transformation of asset management through Fintech.

Stephen Ingledew, Chief Executive at FinTech Scotland said:

“Fintech innovation in asset management and capital markets is a fast emerging trend with a growing number of fintechs in Scotland developing innovative propositions to help the sector be more efficient and deliver better outcomes to investors. THis is being boosted by Scotland attracting many international fintech firms for example Agrud from Singapore and Actelligent from Hong Kong, who are attracted to Scotland because of university research capabilities and highly qualified students and professionals.”

The Scottish Asset Management Market

With £8 trillion AUM (as at end of 2019) the UK is currently the second largest global centre for asset management after the United States. Within the UK, Scotland is the second largest financial services centre after London, and includes the headquarters of Aberdeen Standard Investments – the largest active manager in the UK with a total AUM of £525 billion as of June 2019. Scotland is also a growing centre for fund administration (also referred to as asset servicing’), with strong corporate links with firms based in London and overseas.

Today, asset managers in Scotland include: Aberdeen Standard Investments, Aberforth Partners, Amati Global Investors, Ardstone Capital, Baillie Gifford, Blue Planet Investment Management, Cadence Investment Partners, Cameron Hume, Castlebay Investment Partners, Circularity Capital, Cornelian Asset Managers, Dalmore Capital, Dundas Global Partners, Edinburgh Partners, Kames Capital, Martin Currie, Panoramic Growth Equity, Pentech, Revera Asset Management, RM funds, Saracen Fund Managers, Stewart Investors, SVM Asset Management, Walter Scott & Partners and Valu-Trac. The following are now subsidiaries of larger asset managers based elsewhere: Kames Capital (Aegon Asset Management), Martin Currie (Legg Mason/Franklin Templeton), Edinburgh Partners (Franklin Templeton) and Walter Scott & Partners (BNY Mellon). Firms originally founded in Scotland, like Newton (also part of BNY), still retain a Scottish presence.

In addition, a number of asset managers headquartered elsewhere have branch offices in Scotland including: Liontrust Asset Management, Investec, Janus Henderson Asset Management, Franklin Templeton, BlackRock and Barclays. Lastly there are a number of smaller boutique firms, many of which straddle fund management and financial advice such as; Alan Steel Asset Management, Balmoral Asset Management, Charlotte Square Investment Managers, KPW Investments, Murray Asset Management, Odysseus Capital Management, Par Equity, Rossie House Investment Management, Rutherford Asset Management, Social Investment Scotland, TCAM and Trafford. Together these asset managers manage a mixture of open-end, mandates and closed-end funds for domestic and overseas investors, across a broad gamut of asset classes. The vast majority noted above (if not all) are categorised as active managers’ (that is, they do not track an index). Currently there are no Exchange Traded Fund (ETF) or passive’ (index tracking) providers based in Scotland.

Fintech Innovation is Happening but not Everywhere

We see more innovation in the asset servicing part of the market but again could grow significantly from here. Currently Scotland does not have any investment exchanges upon which to trade assets. Currencies are traded without a centralised location, rather the FOREX market is an electronic network of banks, brokers, institutions, and individual traders (mostly trading through brokers or banks). Scotland has no central clearing companies; for asset managers, the main firms that serve the UK are Euroclear, Clearstream, LCH Clearnet and Calastone. All are based in London or overseas. Similarly all of the large global custodians like State Street, RBC, BNY and Blackrock (that control >90% of the market) centralise their custody operations outside of Scotland. Scottish stock brokers include Redmayne Bentley, Speirs and Jeffries (acquired by Rathbones in 2018) and StockTrade. However the majority of brokerage is controlled by large investment banks like Morgan Stanley, JP Morgan and Goldman Sachs outside of Scotland.

Meanwhile smaller providers like Valu-Trac, based in Inverness, and Multrees Investment Services, based in Edinburgh, offer a range of fund management, administration, custody and back office services. A number of asset managers (e.g. JP Morgan, Morgan Stanley, Blackrock) also base their asset servicing and technology operations in Edinburgh and Glasgow. Computershare is a global leader in financial services and data management, working with around 16,000 global clients and their 125 million customers and having an established operation in Scotland providing relationship management and registry services to around 150 listed companies in Scotland and beyond.

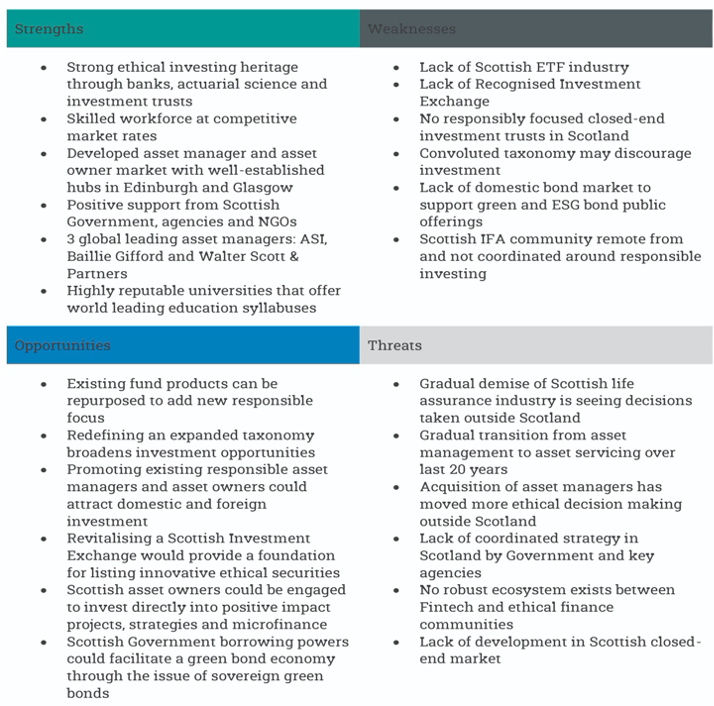

The analysis of the Scottish responsible investing market can be summarised in the following table of strengths, weaknesses, opportunities and threats.

Fig. Extract Mapping the Responsible Investing Landscape in Scotland’.

Page 55: SWOT Analysis’:

Conclusion: A Missed Opportunity

This innovation is not being replicated in the front and mid office of asset managers or asset owners and here the opportunity arises. Scotland lacks many of the traditional levers to stimulate responsible investment. This stymies the size the market could grow to. It also presents as a missed opportunity for Scottish Fintech. The goal is encouraging external investment into Scotland through asset management and asset owners. In doing so to become a global headquarters for responsible investment. Developing technology solutions and platforms to transplant these deficiencies calls on Fintech investment. The dawn of rTech’, responsible and sustainable Technology, with it the New Fund Order’ is set to becoming increasingly Green.

JB Beckett, Consultant, Ethical Finance Hub, Global Ethical Finance Initiative #GEFI #newfundorder #fintechscotland #scotlandisnow #scotlandistomorrow

Co-Author Mapping the Responsible Investing Landscape in Scotland’

Author New Fund Order 2.0 A Digital Resurrection’

Co-Author: The WealthTec Book’, AI Book’ and Paytech Book’

Photo by Karolina Grabowska from Pexels

Diversity up, Inclusion down – Business Impact & Solution

Let’s start with an existential question – why do we even exist as human beings?

An ultimate accomplishment is to have complete and unhindered self-expression. For most of humanity, this happens best in the context of love, respect and belonging since it makes us feel safe and courageous. We also know that the opposite of courage is not fear, it is conformity. And conformity suppresses creativity and self expression.

Honest D&I is an organization’s way of saying “I love you and I respect you” and leaders have the highest leverage and impact of anyone. For some time this has been a space where the answer to the question of being a company that believes in and practices D&I was “we think so”. It does not have to be that way anymore. People Analytics and in particular ONA (organization network analysis) is a tool companies can use effectively, at a relatively low cost in relation to ROI, to visualize, measure and constantly make increments. We will get to this a little later.

Diversity Doesn’t Stick Without Inclusion

As per HBR, “Diversity” and “Inclusion” are so often lumped together that they’re assumed to be the same thing. But that’s just not the case. I”‹n the context of the workplace, diversity equals representation. Without inclusion, however, the crucial connections that attract diverse talent, encourage their participation, foster innovation, and lead to business growth won’t happen. Numerous studies”‹ show that diversity alone doesn’t drive inclusion. In fact, without inclusion there’s often a diversity backlash.

As noted diversity advocate ”‹VernÄ Myers”‹ puts it, “”‹ Diversity is being invited to the party. Inclusion is being asked to dance.”

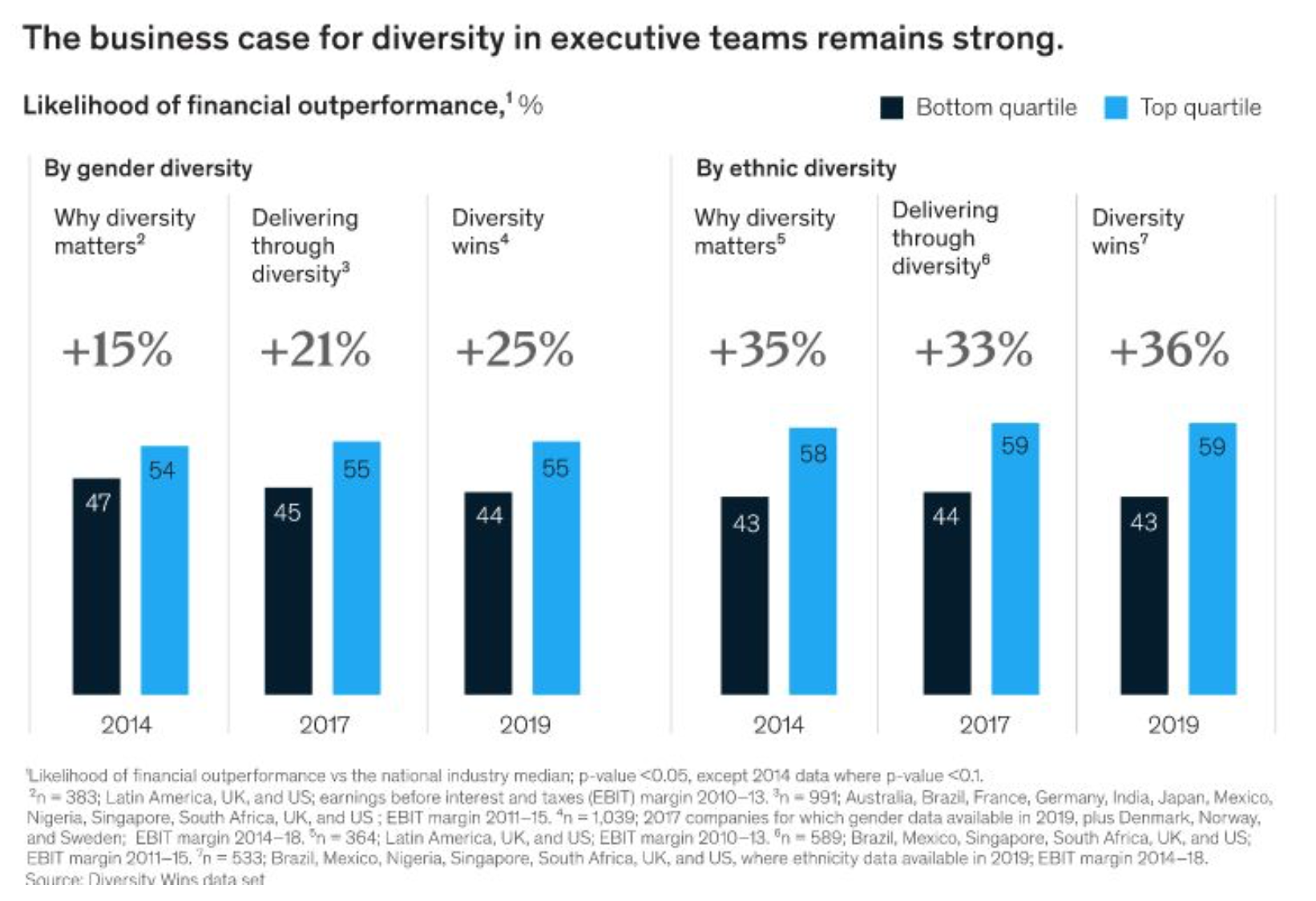

McKinsey has been researching this domain for numerous years. The findings below emerge from their largest data set so far, encompassing 15 countries and more than 1,000 large companies. They have incorporated a “social listening” analysis of employee sentiment in online reviews and their findings highlight that companies should pay much greater attention to inclusion, even when they are relatively diverse.

Diversity – Key Takeaways:

- Likelihood of outperformance continues to be higher for diversity in ethnicity than for gender – a substantial differential likelihood of outperformance””48 percent””separates the most from the least gender-diverse companies.

- The greater the representation of women, the higher the likelihood of outperformance; Companies with more than 30 percent women executives were more likely to outperform companies where this percentage ranged from 10 to 30,

- companies in the top quartile for gender diversity on executive teams were 25 percent more likely to have above-average profitability

- despite the awareness, there is a widening gap between D&I leaders and companies that have yet to embrace diversity; the representation of ethnic-minorities on UK and US executive teams stood at only 13 percent in 2019, up from just 7 percent in 2014

- In 2019, fourth-quartile companies for gender diversity on executive teams were 19 percent more likely than companies in the other three quartiles to underperform on profitability””up from 15 percent in 2017 and 9 percent in 2015.

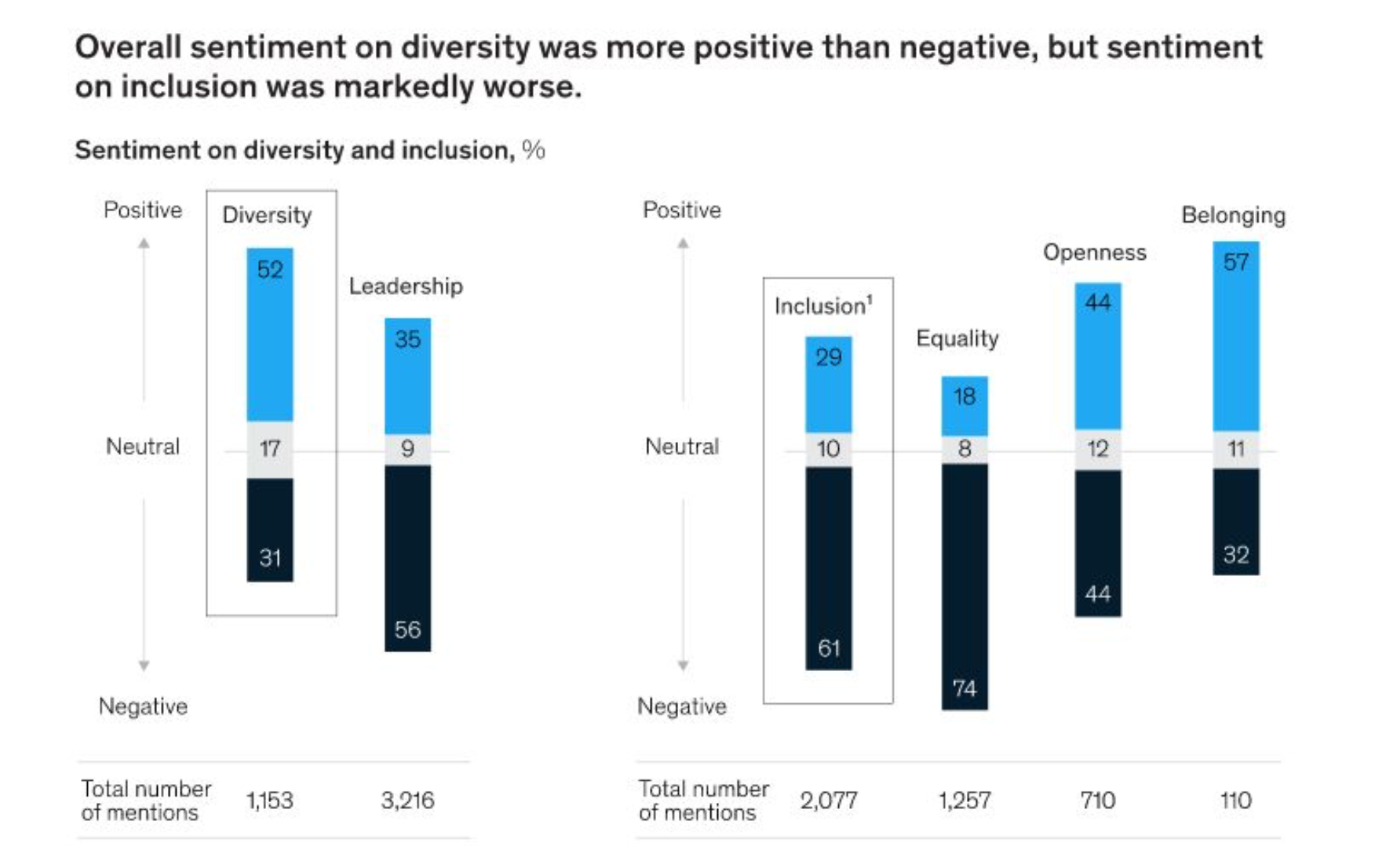

Diversity without inclusion is a story of missed opportunities. Here are some key takeaways from McKinsey’s outside-in research using “social listening,” focusing on sentiment in employee reviews of their employers posted on US-based online platforms. While this approach is indicative, rather than conclusive, it could provide a more candid read on inclusion than internal employee-satisfaction surveys do

Inclusion – Key Takeaways:

- While overall sentiment on diversity was 52 percent positive and 31 percent negative, sentiment on inclusion was markedly worse, at only 29 percent positive and 61 percent negative.

- For the three indicators of inclusion””equality, openness, and belonging”” their research found particularly high levels of negative sentiment about equality and fairness of opportunity.

- Negative sentiment about equality ranged from 63 to 80 percent across the industries analyzed. Negative sentiment about openness ranged from 38 to 56 percent

- Belonging elicited overall positive sentiment, but from a relatively small number of mentions.

HBR research finds that employees with inclusive managers are 1.3 times more likely to feel that their innovative potential is unlocked. And therefore employees who are able to bring their whole selves to work (i.e. who feel included) are 42% less likely to say they intend to leave their job within a year.

Societal Context

Let’s zoom out for a second into a wider societal context. Over 9 million people in the UK ”“ almost a fifth of the population ”“ say they are always or often lonely. The Brits may not be the only ones feeling this way. The overuse of technology is a cause of depression, social anxiety and a lack of meaningful connections. And if we add to this lack of feeling included at work, what kind of a society will we end up creating? This impacts everyone – our own partners, kids, parents. With only a handful of aware individuals (leadership), a world of good can be created in society.

Not only it D&I is right from a humane perspective, but data not only suggests that it makes a good deal of business sense; organizations with the D&I”‹ esprit de corps’”‹ position themselves for business success by attracting the right kind of talent and making them feel like they are in the right place. This spurs safety, feeling cared for and as a result the release of the creative genie out of the bottle for out of the box thinking, non-conformist thinking and exemplary performance. The stats are above to make the business case.

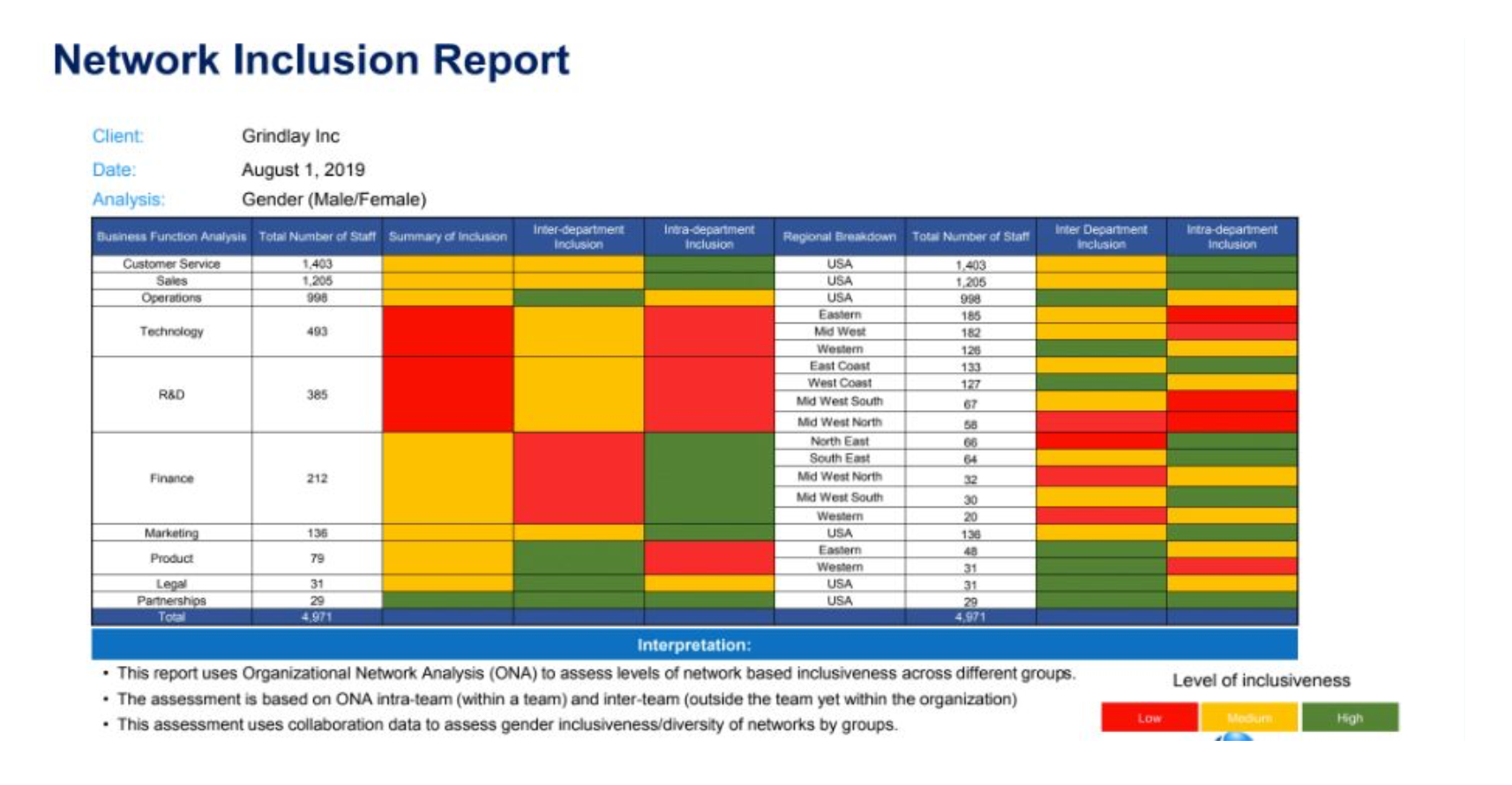

Using Organization Network Analysis for insights into D&I to track and report progress

For some time this has been a space where the answer to the question of being a company that believes in and practices D&I was “we think so”. With Organization Network Analysis (ONA), it does not have to be that way anymore! ONA can be used not only to measure diversity but also to measure network activity and analyze the immersion of different employees across the organization

With ONA, you can map and analyze patterns of interaction across relationship networks of every employee, so Diversity & Inclusion leaders can understand where differences exist in specific groups of employee’s networks in different hierarchies.

Even relatively diverse companies face significant challenges in creating work environments characterized by inclusive leadership and accountability among managers, equality and fairness of opportunity, and openness and freedom from bias and discrimination. However with the right tools, technology and data, you can measure the impact of your various D&I initiatives and make required improvements on an objective basis.

Puneet Sachdev is International Director, Human Capital at The Singularity Lab. The Singularity Lab is an integrated human capital consultancy, helping technology companies achieve exponential results by attracting and retaining top talent and creating high performing inclusive cultures based on data, design and technology. Learn more about our”‹ ”‹ONA solution”‹ for D&I.

Mental Health in the workplace under COVID-19

Coronavirus is inevitably something which has affected us all. It has affected how we feel, how we work, and how we live. We want you to know that no matter how you are feeling during this time, you are 100% not alone. You are completely normal. You are acting like a fully functional human being reacting to threat, and we are all hardwired to do this.

So what is the hardwiring of humans that makes us feel anxious, irritable, and unmotivated during this worldwide pandemic? We explore what roles various parts of the brain have to play in our reactions to this threat. We are hopeful that by gaining an understanding of these functions, we can recognise and respond in ways that will work more effectively for us.

None of us really have any control over the coronavirus spread, or the economic situation. But we can act to help ourselves. We believe that through having structure and routine; acknowledging our thoughts and feelings; practicing mindfulness; becoming aware of our breathing; taking care of our physical needs; and considering our personal values, that we all might be able to take some steps towards improving our mental health during these times.

Below you can find our blog around Mental Health and how OK Positive can help with supporting you individually and your company.