Transforming the Everyday Life of People and Business Through Pioneering FinTech Innovation in Banking

Fintech Scotland announces new strategic partnership with NCR Corporation

FinTech Scotland, the cluster management body, has announced a new strategic partnership with NCR Corporation, a leading enterprise technology provider to further advance innovation for financial institutions.

The partnership builds on NCR’s strong innovation track record as a software and services provider with a long-established heritage of applying new technology developed through its Dundee Discovery Centre.

The announcement follows the recent release of FinTech Scotland’s ground-breaking Research and Innovation (R&I) Roadmap which, developed in conjunction with key players in the financial industry, includes a key focus on the future of payments and transactions and financial regulation.

Spanning more than 130 years, NCR has a rich history of delivering innovative solutions for consumers and businesses. With expertise in payments, transactions, digital banking and strategic advisory services, NCR will join FinTech Scotland and its other thirty strategic partners, including fourteen of the largest financial services firms, to drive forward a customer- and digital-led financial innovation transforming how people, communities and businesses engage with money and finance.

FinTech Scotland, the cluster management body for strategic partnerships within the country, will work closely with NCR, a major employer in Dundee, and its 600-strong financial experts in the region to develop innovation opportunities with fintech firms and financial institutions, plus the wider cluster stakeholders such as universities and innovation centres.

Nicola Anderson, Chief Executive, FinTech Scotland, said,

“We are hugely excited to about the strategic partnership with NCR and their dynamics and pioneering approach to developing technology will further accelerate innovation with fintech SMEs and large financial firms in the cluster. Our industry-driven, action-orientated R&I Roadmap will provide the ideal framework to advance new financial services innovations with NCR and we look forward to the collaboration with the NCR team in Dundee as well as the USA and across the globe”.

Colin Payne, corporate vice president, NCR Professional Services said

“In my experience the value of regional fintech powerhouses is undeniable, bringing raw talent and passion into the space and guiding the development of next-generation financial businesses. In Scotland, this is particularly true given the rich engineering heritage, innovative mindset and history of outstanding customer-focused financial services ”“ this unique combination brings us a new generation of powerful fintechs. We are delighted to partner with Fintech Scotland to support the scaling of these amazing new solutions.“

Rise, created by Barclays, launches new Insights report, ”˜Making data count with AI’

Rise Insights report lead, Grace Batchelor, Rise London FinTech Platform Manager shares highlights on one focus area in the report ”“ ethics in AI.

The latest edition of the Rise Insights report, Making data count with AI’, surveys the data revolution that’s taking place, the role of AI and the opportunities it presents to financial services, including fintechs. In this article, we summarise the drivers of the revolution, and focus on the practicalities of what might sound like a theoretical subject ”“ ethics in AI.

As Ben George, Distinguished Engineer for Data in Barclays Chief Technology Office writes in the report’s foreword:

As Ben George, Distinguished Engineer for Data in Barclays Chief Technology Office writes in the report’s foreword:

“Raw data is rocket fuel, highly powerful but also highly dangerous.”

For individuals, the loss of direct control can be alarming when every click or swipe sees their personal data scattered into a huge number of anonymous corporate data silos around the globe. They must rely on trust alone ”“ trust in those corporations to store, process and share the data properly ”“ when they have only a tenuous relationship with the companies.

Could there be a more transparent protocol of data sharing? At Rise, created by Barclays, we like to think so. Imagine people being able to choose their own data policies from an app, setting time limits on data availability and even fixing a price to sell their data. Several things will bring about this data revolution:

- A combination of technologies, including AI, that underpin the data-sharing vision on a global scale

- Savvy fintechs with innovative solutions in the data space

- Large financial services and technology organisations committed to the new vision

- Modern regulation designed for this new world

Importantly, all parties will also need an appreciation of the importance of ethics in AI, and they’ll need to actively adopt it. Read more about these subjects in the report.

Do no harm: The role of ethics

From customers’ perspective, trust will remain critical. But how do companies do the right thing’ with data to establish trust (and adhere to regulations)? It’s a question that’s in sharp focus given the commercialisation potential of data and new AI technologies.

Katryna Dow is Founder and CEO of Meeco, and contributes an article to the report with practical advice on getting started in the data revolution. She’s confident that “a more citizen-centric approach based on a more equitable and ethical considerations to data is entirely possible given today’s technology.”

In a Q&A section of the report on the ethics of AI, David Bholat, Barclays UK Chief Data Scientist, tells me why we should be rational about AI: “Cancer diagnosis is a high-stakes situation. Although less critical, credit allocation can be scary too. It’s understandable that these make us fear taking the wrong decision. But I think we should distinguish between the scariness intrinsic to those situations, and the application of AI in them. Credit decisions and cancer diagnoses need to be made. We should be pragmatic, and use the best tools at our disposal to make them.” When several studies show that computer vision techniques outperform clinical experts in tumour detection and machine learning can outperform simpler statistical models in underwriting, an objective approach to AI is a sound starting point.

Also in the report, Michael Payne, Barclays UK Data & Analytics MD, shares the five tenets that banks will be held to:

- Transparency: A willingness to explain clearly what they’re doing with their customers’ data

- Control: Giving customers clear rights and easy ways to govern how their data is used

- Beneficiaries: Line of sight on who is benefiting from data usage and what consumers get from this

- Accountability: Checks are in place to ensure AI systems are performing reliably and safely

- C-level focus: Fostering company board discussions on ethics, especially around edge use cases

The Q&A section also covers other ethical topics including some important aspects of data cleansing, how a type of deep learning, Generative Adversarial Networks, can alleviate privacy concerns and why AI and data commercialisation is shaping new data products and services.

Fintechs featured in the report

In realising new commercial opportunities, banks and other financial services institutions can follow the lead of agile and innovative fintechs and smaller tech ventures. The report includes contributions from the following:

- AlphaStream: End-to-end hyper-personalised user experiences for financial services

- EntropikTech: The world’s leading Emotion AI platform that reads human emotions and helps brands redefine their offerings and experiences

- Flybits: Empowering banks to engage an audience of one, at scale

- GV (formerly Google Ventures): Backing founders who transform industries and create new ones

- Maven Securities: Building new trading technology to ensure fast, efficient and transparent market access

- Harbr: Delivering refined customer experiences, high-value products and new revenue streams

- HolisticAI: Software solutions for AI risk management and auditing

- Illuminate Financial: A thesis-driven venture capital firm dedicated to enterprise fintech and B2B software companies

- Level E Research: Edinburgh-based startup creating autonomous machine learning investment solutions scaled for the platform economy

- Meeco: The infrastructure for trusted personal data ecosystems

- PolyAI: Building enterprise voice assistants that carry on natural conversations with customers to solve their problems

- ProGrad: Credit risk assessment platform connecting financial institutions with third-level students

- Quantexa: Creating a new generation of decision intelligence built on context

- vPhrase: Lets enterprises create highly personalized language-based reports at scale, at machine speed

Get involved

We’re all central to the debate on how individuals harness the value of their own data.

“Think about ethics now and AI can empower rather than oppress us.[1]” ”“ Sir Nigel Shadbolt, Principal of Jesus College, Oxford and Professor of Computing Science, Department of Computer Science

- Download the Rise Insights report to learn more about how AI adds value to data

- Register for an Ethics in AI event that Rise is running in conjunction with our colleagues at Barclays Eagle Labs

- Contact the Rise team in London or New York to meet any of the companies featured in the report or in the Rise ecosystem of over 100 FinTech startups

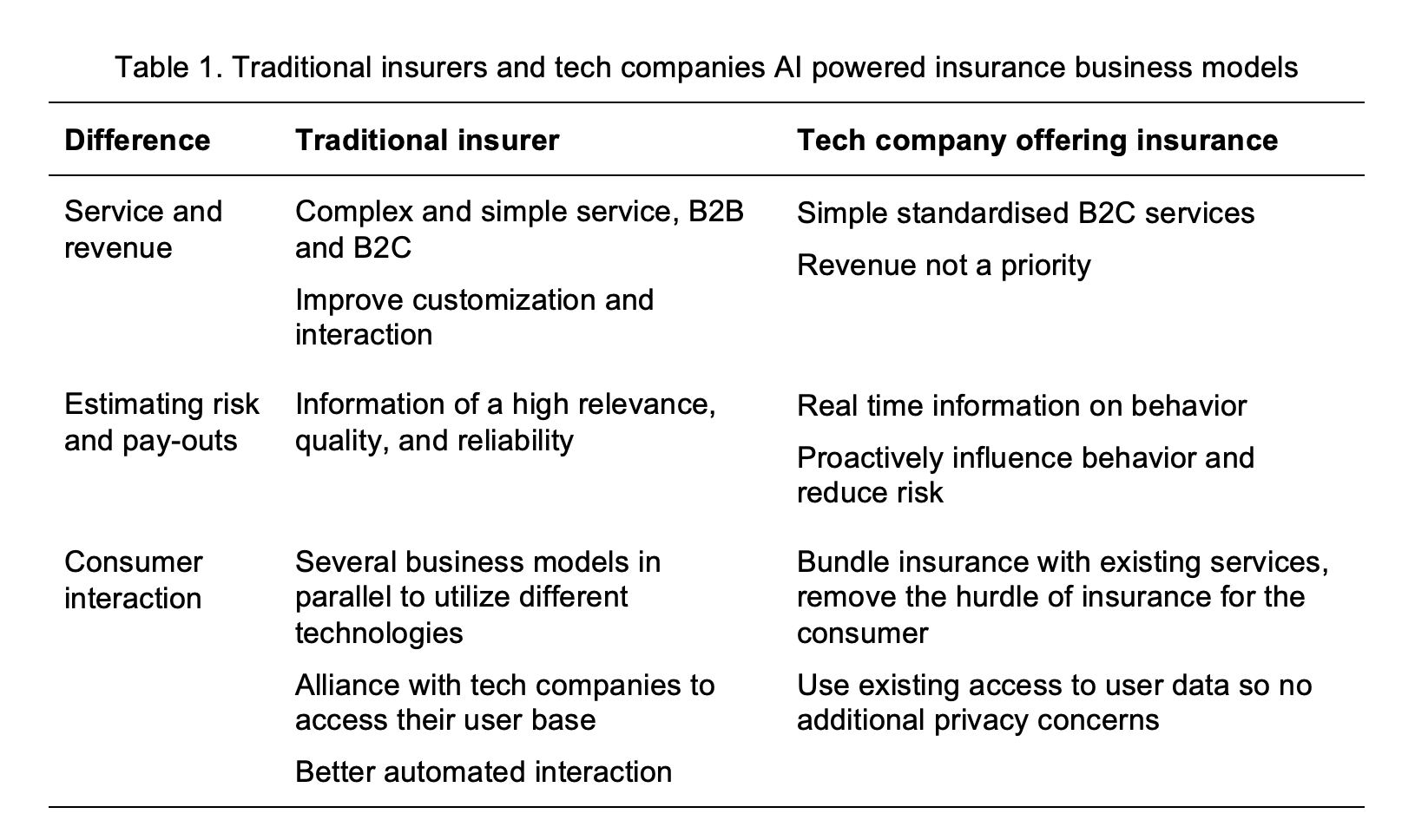

Existing insurers and disruptors are utilizing Artificial Intelligence to create new business models

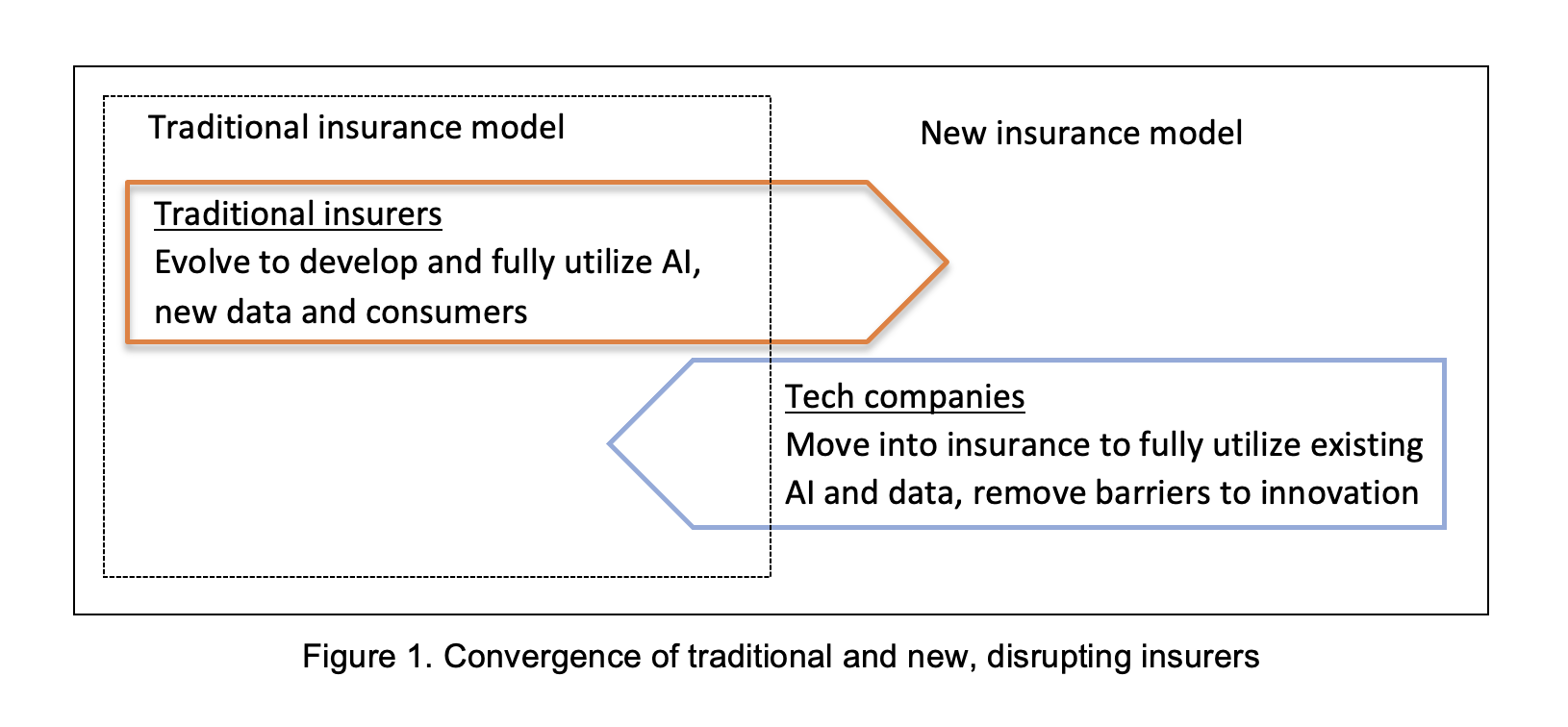

We can see that Artificial Intelligence (AI) is transforming many parts of our lives, but do we know where this journey is taking us? Insurers need some certainty on what their future will looks like. Some new insurers are trying new business models enthusiastically and then changing direction sharply, like a speedboat swerving to avoid a collision. The larger insurers, however, are like large cruise ships; they need to be able to see far ahead before they plot their course, and they don’t want to keep changing direction.

This research tried to identify the viable AI driven business models to help give some clarity. Some traditional insurers are just trying to be more effective with AI, while others reinvent themselves to fully utilize the new capabilities available. Tech-savvy companies from outside the sector like Tesla, are entering and disrupting it. Would these diverging paths continue, or would they converge in the future towards one, ideal, business model? This research focused on one example of a traditional insurer and one new tech-savvy disruptor and evaluated whether their models are converging.

AI is changing the insurance value chain, as illustrated in figure 1. Most new insurers, like Tesla, offer fully automated simple services. The traditional insurers offer some of their simpler services in this way. The more complex services are supported with AI, but a human makes the final decision. An example of this are audits for fraud, where the AI identifies unusual patters and cases for an expert to evaluate.

There are signs of convergence between the models of traditional and new insurers. First, there is convergence in technologies, such as the use of chatbots utilizing AI. Second, there is a convergence in processes, for example, the interaction with the consumer. Third, there is convergence in the strategy on costs and pricing.

However, there are two areas where there seems to be a limit on convergence, which seems to suggest the business models of the incumbent and the disruptor will remain distinct. These are: (1) evaluating risk and (2) the cost of attracting the user and profitability.

Despite some convergence, certain differences are likely to remain even after this transitionary period. This is because the two models have distinct competitive advantages. Traditional insurers no longer monopolize the capability of providing insurance, but they still have the existing user base and utilize it to evaluate risk. Technology-savvy companies that now offer insurance, have their own forms of engagement with their consumers, use different methods to evaluate risk due to their access to real time data, and do not prioritize generating revenue but instead utilize insurance to increase their user base, overcome barriers, and reduce the overall cost of their products and services.

Therefore, when insurers are thinking about how to utilize AI and plot their course through the turbulent, unpredictable times ahead, they should stay true to what they are. This is their comparative advantage.

Dr Alex Zarifis is a lecturer at the University of Nicosia in Cyprus.

This article is adapted from his paper, “Evaluating the New AI and Data Driven Insurance Business Models for Incumbents and Disruptors: Is there Convergence?” available from https://doi.org/10.52825/bis.v1i.58.

The future of automation for UK asset managers

The last 18 months have been amongst the most disruptive that the financial services industry has ever experienced, forcing many sectors to reconsider business models.

Asset managers in particular have undergone a substantial transition as video conferencing has replaced client-facing interactions. To better understand how these firms have responded to market disruption, we surveyed 100 Heads of Operations across UK asset management firms to learn about their operational challenges, automation objectives and plans for regulatory compliance in 2022.

From this study, three lessons stood out for their relevance to the wider fintech industry:

1. Operational challenges and tech improvements are company-specific

We asked asset managers what does and doesn’t present a challenge to their daily operational processes.

While the availability of automated systems and adequately skilled staff were highlighted by two-thirds of respondents as the most significant challenge, firms also pointed to many others including the functionality of manual resources, process complexity and a changing regulatory burden.

Although nearly 8 in 10 acknowledge that the capabilities of current systems are hindering operational growth, firms have identified a range of priorities to improve these systems from seamless data flow, AI-assisted dashboards and dynamic data management through to enhanced risk management and talent acquisition.

The variety of responses tells us that no two firms face the same operational challenges and, consequently, that technology infrastructure improvements for 2022 will be equally varied in their application to the asset management industry.

2. Manual reconciliations continue to challenge asset managers

Reconciliation is an essential process for keeping accounts and financial records accurate. In recent years, more firms have been automating reconciliation procedures to eliminate risk of error and improve accuracy.

Despite this, our survey reveals that:

- 60% of asset managers worry that manual reconciliations are the greatest risk to their organisation

- 75% say that the number and volume of manual processes is an immediate operational challenge

- Only 7% say that manual processes present no challenge to their firm

Data preparation was also highlighted amongst the most time-consuming tasks for businesses, which further highlights how the complexity of data management continues to grow year on year. This is consistent with our work across other sectors, where we find that manual processing is really the core issue underlying poor reconciliation disciplines.

With half of UK asset management firms allocating budgets between £0.5 and £10m to address manual inefficiencies, we can expect automation to become more deeply embedded in the industry throughout this year.

3. Regulation is accelerating the trend towards automation

Although manual processing has been steadily declining for years in favour of automation, our findings show that a growing regulatory burden is definitely a factor in this transition.

Just 2% of asset management firms in the UK have no plans to invest in automation to achieve regulatory compliance. For the majority that did, top focus areas include operational resilience, prudential regulation, MiFID II and CASS. A further 7 in 10 felt that automation will be instrumental in achieving compliance with the IFPR regulation, which came into effect on 1st Jan 2022.

These findings tell us that UK firms are actively pursuing automation as a convenient and cost-effective way to fortify against regulatory breaches. Nevertheless, with 42% still pointing to new or changing requirements as the biggest threat to their company, such solutions need to be flexible as requirements continue to grow in scope and complexity.

What does this mean for software providers?

The results of our survey clearly demonstrate that automation in finance will become ubiquitous in the medium to long-term. However, the variety of responses and priorities outlined also shows that firms do not want an off-the-shelf solution; instead, they want a reconciliation platform which:

- Is configurable to specific operational needs

- Eliminates manual intervention through end-to-end automation

- Is purpose-built around specific regulatory requirements

- Is flexible to accommodate for multiple iterations of regulations

Of course, these are welcome findings at AutoRek, where we have spent over two decades working with financial firms to build bespoke solutions for unique reconciliation, operational and regulatory requirements.

In the short-term, it is clear that asset managers recognise how automated reconciliation disciplines do and will continue to form the cornerstone of an effective business model in today’s post-pandemic environment. It will be interesting to see how this plays out across the wider financial industry over the next 12 months.

Photo by George Morina from Pexels

Edinburgh named as one of the UK’s leading tech cities

Edinburgh has been named as a UK’s leading tech cities in the UK thanks to its combination of high levels of VC funding, available tech job, advertised tech salaries, number of current and future high-growth tech companies, according to new analysis for the UK’s Digital Economy Council.

Rewarding skilled tech talents

In Edinburgh, skilled tech talent can see job offers with salaries averaging £58,405 for a new role. This is the highest in the UK outside of London and the South East. There are now over 2,000 tech job vacancies in the city, an increase of 85% since last year.

Sandy McKinnon, Partner at Pentech Ventures, said:

“Edinburgh has steadily been growing as a tech hub over the past few years and this list recognises that. The combination of world-class universities, established IT businesses and unicorns like Skyscanner and FanDuel means there is a lot of exciting talent and innovation in the city. We’re seeing this with newcomers like TravelNest, Desana, Amiqus, Biomage and many others that are disrupting traditional industries – there really is so much potential around the city.”

Investment

Tech companies in Edinburgh have raised £117 million through 47 venture rounds, the second highest number of rounds in the UK. These include health tech Current Health (£32.5), foodtech Parsley Box (£17m), and tidal energy company Nova Innovation (£6.4m).

30% of new unicorns created this year I the UK are established outside of London, including Interactive Investor in Glasgow.

Digital Minister Chris Philp said:

“It’s brilliant to see Edinburgh ranking in the top five regional cities for UK tech, with innovative Scottish startups helping tackle some of the world’s major challenges.

“Capitalising on this brilliant growth across the whole of the UK is part of our mission to level up and we are supporting Scottish companies with pro-innovation policies to help people and get the skills they need.”

Levelling Up Power Tech League 2021:

-

Cambridge

-

Manchester

-

Oxford

-

Edinburgh

-

Bristol

-

Leeds

-

Birmingham

-

Newcastle

-

Cardiff

-

Belfast

Photo by saifullah hafeel from Pexels

An end of year “Thank You” message from our CEO

As we come to the end of 2021 and look forward to 2022, we’re reflecting on the year and are hugely proud of what’s been happening across Scotland’s FinTech Cluster. Despite the continuing challenges from the COVID-19 pandemic we’ve seen fintech SME Growth, both in number of businesses and in terms of scale, we’ve seen record levels of investment in Scottish fintech SME’s, a true testament to the calibre of the businesses and leaders who continue to inspire us day on day.

The past twelve months have also seen more international growth with up to 50% of Scotland’s fintech SME’s building plans for international trade and more global businesses locating to Scotland as they establish a UK base.

We’ve also had the Kalifa review of UK fintech acknowledge the established progress of Scotland’s FinTech Cluster, and we’re looking forward to supporting the implementation of the Scottish Technology Ecosystem Review led by Mark Logan and building a plan to enable Scotland’s future digital economy.

The FinTech Scotland festival provided us all with an opportunity to meet again face to face and if we needed it, it reinforced the energy, optimism, diversity of contribution and breadth of collaboration that contribute to our fintech successes. A highlight for all of us in the FinTech Scotland team were the hybrid and in person events, kicking off with the DIGIT FinTech summit and ending with the Times and Futurescot event where we welcomed the UK regional fintech clusters to Scotland in the Accelerating UK FinTech conference.

During 2021 we have seen a growth in climate fintech, with new fintech SME’s starting to develop businesses to help address the impact of climate change and support the journey to net-zero, as well as established fintech SME’s expanding their existing capabilities to tackle this important issue. I have no doubt we’ll see more of this in 2022 and we’re looking forward to doing more to stimulate and accelerate climate fintech in Scotland.

With the establishment of the Scotland fintech SME advisory Board we have a clear plan on fintech SME priorities for 2022, and it is a privilege to work with these dedicated leaders who have come together aligned behind the vision of economic, social, and sustainable growth across the FinTech Scotland Cluster.

Looking forward to 2022 we’re focused on supporting fintech SME’s to scale and grow, strengthening international connections, building more impactful fintech collaborations and deliberately driving more fintech Research and Innovation (R&I) in Scotland and across the UK. We plan to launch the FinTech Scotland R&I roadmap early in 2022. It’s a plan that pulls together industry R&I priorities as we ask ourselves, what should finance look like in 10 years-time, and it provides us with a framework to lead the answers to that important question.

In drawing to a close, I’d like to say thank you to everyone that’s supported the FinTech Scotland Cluster across 2021. I’m continually reminded of the privilege it is, to know you and work with you in our collective efforts to lead and achieve our ambitions for fintech in Scotland. I’d also like to say a special word of thanks to the brilliant team at FinTech Scotland. I see their energy, commitment and drive everyday and it’s a pleasure to work them.

My final note is to wish you all a happy and healthy 2022 and we’ll look forward to seeing you all next year as we continue to build on our plans and drive the FinTech Scotland Cluster.

82% of 50s market would not take robo-adviser financial advice

New research from Visible Capital on the over 50s market shows that 82% would not take financial advice from a robo-adviser and 88% would not be willing to give details of their finances to a robo-adviser to enable them to give a better personalised service.

The results come from new research carried out amongst UK adults with an age range from 50 upwards, with the bulk of the respondents aged 60 to 80. 38% said they currently access financial advice through an adviser or accountant.

This aversion to pure digital advice was amongst a cohort of whom over 60% said they had been relying on technology more during the pandemic period and are comfortable with technology and have clearly adapted well to navigating the huge range of interactions and services which have gone online during COVID19.

Among the group, 84% were using online services for general banking, 52% for insurance, 44% savings and investments, 64% for payments and transfers and their 55% were managing their credit cards digitally. Yet only 15% of respondents used online services for advice.

A fifth (20%) of respondents said they trusted technology less coming out of the pandemic; perhaps some of their digital encounters have been frustrating and only borne of necessity.

Ross Laurie, CEO Visible Capital, comments:

“This should be interesting reading for financial advisers being a wealth cohort of which 64% said they felt reasonably well off’, which for the majority of advice firms will sit squarely within their core client group.

The results of our survey show that age 50+ savers and investors are no strangers to using digital services, which has been accelerated by the pandemic and is likely to grow in the post pandemic world. But, as yet, they have not taken advantage of online financial advice. Our survey results show that trust is a major factor here. Utilising the tools and services with which this group are already familiar ”“ online banking, investing, saving, etc, ”“ advice firms can offer this day-to-day technology with the kind of personal, trusted human advice which many of them already value.

Advisers have a real opportunity to step into the hybrid advice space and claim it as their own.”

Scotland Fintech festival! We loved it and can’t wait for next year!

We recently concluded the FinTech Scotland festival ending a wonderful four weeks where we got to celebrate fintech innovation in Scotland, across the UK and around the world!

With 60 events covering a broad range of interesting topics, discussions, and views for the future there was plenty to talk about and more to excite us for the next 12 months ahead.

We started in Edinburgh and ended in Glasgow taking a trip around the world via Australia, America, Europe, Dundee, Stirling and London!

Among my favourites were the face to face events, where the buzz and energy in the room confirmed there’s much going on in FinTech innovation in Scotland, and that we all were excited to be out and about reconnecting face to face, enjoying new conversations and sparking new ideas.

Digit’s FinTech Summit kicked everything off in true Digit style. It was great to see Visible Capital, LendingCrowd, Amiqus, Sustainably, ShareIn, Zumo, Nude, Exizent and Love Electric, all Scottish home grown fintech talents, building and scaling businesses, and developing the future of finance.

Other one of my favourite events was a truly brilliant and informative discussion on the meeting of Space Data and FinTech! Thank you, the University of Strathclyde, Trade in Space, Go-to-Market for sharing your insights, experience and expertise on how Space Data gives us an exciting prospect for more fintech innovation!

FinTech innovators never fail to inspire me, it was an privilege to share an event that saw Know-it, Doqit, Biscuit Tin, PolyDigi and Gigged.ai talk about their businesses, innovations and aspirations for the future.

We connected around the world, sharing experiences of Open Banking innovation with FinTech Australia and hearing directly from a range of European regulators on their experiences of fintech.

Our own regulator the FCA hosted a record number of events covering topics from crypto, Innovation, Sustainable finance and RegTech!

We rounded the festival off in Glasgow with the Times Scotland and Canongate event and an opportunity to discuss accelerating fintech across the UK! Another event that reminded me of the value of connection, the true potential for UK fintech innovation and role that Scotland plays in influencing that story and setting direction.

Thank you for joining us, being part of our story and helping us to shape the future.

Fintechs empowering SMEs

Season 1, episode 11

Listen to the full episode here.

The fintech movement hasn’t just disrupted the way customers and citizen deal with money and access financial products or large financial institutions digitise themselves. Fintech is transforming how SMEs work and organise themselves.

In this episode we’ll explore how fintech is transforming SMEs. We’ll discuss adoption rates, opportunities and challenges faced by fintechs trying to sell their solutions to SMEs. Can collaboration with trusted financial institution be the solution to mass adoption. We’ll also look at ahead and explore future trends.

Anthony Persse – CEO at Optimum Finance

Lynne Darcey Quigley – CEO and Founder of Know-it

Derek Smith – Head of Digital Solutions at Virgin Money

The evolution of high-growth tech firms in Scotland

By Lynsey Walker, dispute resolution partner and tech specialist at Addleshaw Goddard

Technology and digital innovation have played an important role throughout the pandemic, which rapidly accelerated a global reliance on connected services.

Digital innovation has protected many businesses which, despite traditionally not being online operators, have been able to pivot through a technology-first approach, providing business continuity which previously would have been an expensive challenge.

As the wider economy opened as Scotland was moved to level 0, our continued ability to work from home while also remaining connected with friends, family and social groups underlines how vital technology and digital innovation is to the country’s economic recovery. It is clear that the loosening of restrictions is not going to result in a return to all of our pre-pandemic practices.

Central to this is the understanding that tech underpins all sectors, from education to manufacturing, rather than a standalone stream supplying businesses with IT or other more traditional machines.

In recognition of this, the Scottish Government has made more funding available to help businesses take advantage of digital technologies to improve their productivity, increase their resilience and create new market opportunities. An additional £11.8 million, announced in November 2020, will go towards helping businesses to adopt digital technologies and improve their digital capabilities.

Looking at the fintech sector specifically, Scotland already boasts one of Europe’s most successful offerings and is projected for notable growth in the years ahead. Innovators are looking to the future and are driving a collaborative agenda in a bid to make impactful change across the sector and for consumers alike.

The launch of the Kalifa Review earlier this year marked a significant milestone for the UK fintech sector, as it set out a strategy that will accelerate growth over the next three years – again enabling post-pandemic recovery.

Deservingly, Scotland was earmarked as a standout region thanks to the continued development of its Fintech Scotland Cluster model. With input from Fintech Scotland, the Kalifa Review sets out a five-point plan to leverage innovation through a positive regulatory environment, developing diverse skills, facilitating investment to scale enterprises and accelerating a targeted approach to inward investment. It will be fascinating to see how we gather momentum in enabling this through investment, innovation and job creation.

Just last week, UK Government ministers were given an exclusive glimpse into the evolving Scottish fintech community as part of an event hosted by FinTech Scotland. Secretary of State for Trade, Liz Truss, and Scotland Secretary, Alister Jack, paid a visit to the Bayes Centre to meet some of the companies driving the thriving fintech ecosystem.

Over the last five years, Addleshaw Goddard has developed its AG Elevate programme, designed to accelerate start-ups and guide fast-growing tech firms through the legal challenges they face. We’re proud to have supported more than 30 fintech and technology entrepreneurs’ innovative businesses, helping many go on to operate internationally.

Originally designed for fintech firms, this year Addleshaw Goddard welcomed all high-growth tech businesses to the scheme and has also placed a greater focus on businesses with an emphasis on sustainability.

Given Addleshaw Goddard’s experience and insight into the tech sector, this year we also launched the Aspiring Unicorns campaign to support high-growth tech firms. We are encouraging as many businesses and entrepreneurs as possible to get involved.

Aspiring Unicorns comprises seven critical lessons for high-growth technology firms to consider such as data, disputes, IP and investments, and we will be delivering relevant insights on these themes over the coming months.

We’ve developed our support programmes as we recognise the supportive infrastructure, innovation and opportunities that are all available within Scotland for high-growth tech and fintech firms. While the last year has been challenging collectively, tech and digital innovation’s positive influence throughout has reinforced why we are committed to championing its capabilities.

Collaborative leadership, entrepreneurial mindsets and support from government is required for Scotland to spearhead the fintech sector at a global level, and it’s evident that we have these tools to continue such drive.

For more information about the Aspiring Unicorns programme, visit: https://www.addleshawgoddard.com/en/insights/insights-briefings/2021/general/guide-aspiring-unicorns-supporting-high-growth-tech/