Transforming Lives with Financial Data: Smart Data Foundry’s Mission

In today’s rapidly evolving world, where data has become the lifeblood of progress, there is an ever-increasing need for reliable insights to drive informed decision-making. The ability to access and analyse vast amounts of data can revolutionise our understanding of complex challenges and pave the way for innovative solutions. In this regard, Smart Data Foundry has emerged as a leading force, spearheading the mission to unlock financial data’s power and transform how we improve lives and shape our societies.

Empowering Financial Innovation

We are a mission-led organisation at the forefront of a paradigm shift. Our purpose is clear: to inspire financial innovation and enhance the lives of individuals by harnessing the potential of financial data. We have established a collaborative ecosystem that empowers decision-makers to leverage data-driven insights for transformative change by forging partnerships with the public, private, and third sectors.

One of the primary motivations behind the creation of our organisation was the realisation that critical policy decisions and strategic actions are sometimes made based on limited or outdated information. This lack of comprehensive and real-time data undermined the efficacy and impact of these decisions, impeding progress and leaving vulnerable populations at risk. We sought to address this gap by developing interactive dashboards that provide near real-time insights into the dynamics of the financial landscape.

Unparalleled Access to Financial Data

Our data-sharing partnerships provide unparalleled access to a wealth of financial data, including a weekly feed of transactions from 1.2 million current accounts across Great Britain through our key partnership with NatWest Group (NWG). This aggregated data allows for the categorisation of income, financial commitments, and essential expenditures every week. Furthermore, with the capability to segment the data by geography, age, and sex, we can equip decision-makers with detailed insights to comprehend the effects of policy interventions on diverse demographic groups.

The importance of such insights is vital to enabling strategic interventions, particularly when it comes to highlighting the experiences of vulnerable and low-income groups. By delving into financial data, we can shed light on the challenges these marginalised populations face, amplifying their voices and paving the way for more inclusive and equitable policies.

This has been recognised by the First Minister, Humza Yousef, I’ve been told about the excellent work that East Renfrewshire Council is doing in terms of their cost-of-living dashboard. Data, we know, if used correctly, if used appropriately, if used wisely, can be one of our greatest tools in terms of how to target our resources where they’re needed the most.

Measuring the Impact of Policies

The impact of policies and interventions is more expansive than their initial implementation. Our interactive dashboards play a crucial role in enabling the public sector to understand and measure the effectiveness of these policies over time. By providing regularly updated insights and the ability to analyse data weekly, decision-makers can assess the outcomes and consequences of their actions. This retrospective analysis allows for a comprehensive understanding of the long-term impact of policies, facilitating evidence-based adjustments and refinements for continuous improvement.

Addressing the Cost-of-Living Crisis

In recent times, the world has been hit by an unforeseen crisis the sharp spike in inflation and energy prices that has left governments and local authorities grappling with its socio-economic ramifications. Consequently, local authorities face the arduous task of adapting to these challenges and making informed decisions promptly. In this scenario, the role of data and actionable insights becomes paramount.

By developing the Cost-of-Living Dashboard, we recognise the urgent need to support local authorities during this cost-of-living crisis. This powerful tool integrates near real-time financial well-being indicators with contextual information, providing local authorities with a comprehensive understanding of the difficulties faced by their citizens.

Informed Decision-Making

Armed with this knowledge, local councils can make more informed decisions and allocate resources where they are most needed, ensuring that their actions have a meaningful and positive impact on the lives of their constituents. The Cost-of-Living Dashboard empowers local authorities to navigate these challenging times effectively.

A Collaborative Approach

Collaboration is crucial to success. We know this all too well and value it highly. By combining the expertise and knowledge from the public, private, and third sectors, we have created a collaborative ecosystem that provides decision-makers with a wealth of insights and knowledge. This culture of innovation and progress inspires us all to work together towards a better future.

Shaping the Future

Our mission is a powerful example of the immense possibilities that financial data holds in promoting positive change. Our organisation’s commitment to providing real-time insights, forging partnerships with key players such as NatWest Group, and addressing urgent issues like the cost-of-living crisis demonstrates our unwavering dedication to improving lives and societies.

In a world where data is the currency of progress, we hope to pave the way for a brighter future. With our mission to inspire financial innovation and enhance the lives of individuals, we are trying to redefine how we approach complex challenges and improve our societies.

Photo by luis gomes: https://www.pexels.com/photo/close-up-photo-of-programming-of-codes-546819/

How to manage retirement during a cost of living crisis

Confused about your pension? You are not the only one. “People have an average 11 small pots, they don’t really know what that means for them in terms of what their retirement income is likely to be,” explained Laura Trott, UK’s Minister for Pensions at a recent evidence hearing by the Work and Pensions Committee examining DWP’s plans to introduce Pensions Dashboards.

And it’s not only UK citizens who don’t know what their retirement income is likely to be. The DWP admitted in the same evidence session that there have been underpayments to the tune of £1bn in state pension payouts due to missing information from people’s national insurance records.

Meanwhile, the cost of living in the UK is rising. The latest inflation figures show prices have gone up by 7.9% in June, with food prices increasing by 17.4%, resulting in 57% of households reporting to have struggled to pay for essentials. This state of affairs has dramatically diminished the capability of people to save for their retirement.

During these worrying times of rising prices, people have much more of a need to know what they are likely to have in retirement. Yet at the moment it’s very difficult to determine what that will look like. This is particularly relevant for younger generations. How millennials go about saving for a pension has radically changed from when their grandparents dealt with retirement. There is a concern that Generation Y (millennials) is not informed enough about saving for a pension, especially considering it is likely they will on average hold more than ten jobs before they retire.

A different pension approach is needed.

Introducing the (delayed) Pensions Dashboard

The UK Government is focused on the financial wellbeing of people by equipping them to be more financially informed and make the most of their money and pensions. This is why the UK Government has initiated the implementation of the Pensions Dashboard, enabling individuals to find and view their pensions all in one place, bringing more awareness to how much they will need to save in the long term for retirement.

Although the DWP recognises the importance of the Pensions Dashboard, it nevertheless announced a delay to implementation:

“The pensions dashboard will play a really important role in bringing that all together and also allowing people to see this alongside their state pension to get a full picture of what it’s going to look like for their retirement,” said pensions minister Laura Trott. “[Yet] it was the issue that we had around the connection process, which was needing more work in terms of the industry and there was insufficient testing in terms of the actual architecture itself. We needed more time to ensure that it was robust.”

The DWP is hoping to have the portal up and running “very soon” and the government body will start the process of writing later this year. This timing, however, has not come soon enough for Jonathan Hawkins, Principal Consultant and Pensions Expert at Bravura. Bravura has been collaborating closely with the Pension Dashboards Programme (PDP), regulators and its industry partners to make sure dashboards are delivered successfully for the good of the industry.

Bravura recently completed a collaboration with MoneyHub at this year’s PASA Annual Conference, at which a fully operational front- and back-end pensions dashboard was showcased for the very first time, demonstrating the tech works. Nonetheless, the pension solution provider is waiting for final guidance from the PDP to continue onboarding clients and build on the work the sizable amount of work the industry has already delivered.

“We are concerned that any further delays in connecting to the CDA will likely eat into the time pensions providers and schemes have to deliver, so it is important the programme comes back online sooner rather than later,” explained Hawkins. “Although June’s announcement played a useful role in tidying up the regulations and legislation around the PDP, we are roughly four months on from the programme reset and we’re still waiting on key guidance on connections and staging deadlines.

“When the guidance is received (which we hope to be over the next few months) there is, of course, a worry that guidance differs in gravity from legislation. It will ultimately be up to the industry to lead by example and to the regulators to ensure appropriate measures are in place to meet the updated timelines.”

In the meantime prices are likely to continue to rise, which puts people more at risk of not putting enough aside for retirement. The Pensions Dashboard is expected to help many, especially the younger generation, in planning for their retirement income in the future. Once it’s ready.

Photo by Breakingpic: https://www.pexels.com/photo/gold-colored-coins-near-calculator-3305/

New signposting service to support vulnerable customers

National Support Network’s directory of national services, Support Hub, has been added by the FCA to the Digital Sandbox and promoted in the FCA Consumer Duty TechSprint. Its ease of use, quality and scope was also praised in a recent Institute and Faculty of Actuaries (IFoA) publication as a solution to enhance customer journeys and support vulnerable customers.

Engaging with a customer who is experiencing the loss of a car, their health, facing problems such as bereavement or redundancy or marking a major turning point in their lives such as becoming a parent can become key moments in which banks or insurers can make a difference to that customer’s wellbeing and resilience. The challenge, of course, is in how to support that customer in a way that is comprehensive and consistent.

National Support Network (NSN) equips organisations with the tools to refer customers to external support services, including charity helplines across 1,000 problem areas. Another unique aspect are the new insights on the challenges facing customers, which can then help firms develop more targeted customer wellbeing and communication strategies.

Co-Founder and CEO, Cat Divers explains:

“Following a background as a chartered insurance professional, I struggled to find support for myself and others. These personal experiences led me to start this initiative to help others facing similar struggles.

Our focus is on making it easy for organisations to refer those in need to specialist support by providing high-quality information. We reduce the noise and streamline referrals by hosting the UK’s largest vetted and independent directory of services.”

Support Hub is one-of-a-kind and can easily be integrated with existing customer platforms and processes through API, iFrame, portal and other offerings. Whereas existing signposting resources can quickly become outdated, or do not offer as much scope, the NSN Directory is continually updated, in recognition of the continually changing support landscape.

Offering a valuable extension to wellbeing strategies and toolkits for both customers and staff, NSNs innovative specialist signposting services can help direct people to charities or third parties who can provide relevant support without risking advisers overstepping their training.

11.8 million people in the UK struggle to find support when facing personal life challenges. Of these, two in five will delay or give up looking (Censuswide, 2020). This is a long-standing issue spanning many areas such as money, health and housing problems. Without finding support at the earliest opportunity, problems are likely to worsen and give rise to yet further problems.

Frontline staff often interact with customers who present multiple requirements and problems. The frequency of these more complex interactions is on the rise as customers grapple with one crisis after another. While specialist teams can support vulnerable customers, many advisers do not have adequate resources to refer customers to trusted support across the variety of problems that can arise.

Customers are facing more varied and complex problems, and the fintech sector is well placed to look for innovative ways in which they can better support their customers in need through these difficult times. As an independent and reliable source for information on external services, the NSN Directory can quickly become an important part of a customer advisor’s toolkit.

National Support Network is a not-for-profit social enterprise.

For more information please see nsn.org.uk

Consumer Duty and fintech innovation

Season 3, episode 4

Listen to the full episode here.

In July 2022, the FCA published its Consumer Duty. Regulated firms need to implement the new rules by the end of July 2023 for open products and July 2024 for closed books of business.

Firms will need to review their products, communications and customer journey.

It will impact most areas in those organisations such as governance, reporting, product design, pricing, distribution, servicing and staff training.

In this podcast we will review the key principles, ask ourselves what the impact on both established firms and fintechs is as well as exploring innovative technologies that can help adhere to those new rules.

Guests:

Venetia Jackson – Senior Associate at Pinsent Masons

Joseph Twigg – Founder and CEO at Aveni

Chris Ansara – Founder and CEO at docStribute

New fintech collaboration to tackle cost of living crisis

In collaboration with Scottish fintech Inbest, NatWest Group has launched a benefits calculator for its customers. The tool allows people to see what benefits they could be entitled to and offers personalised signposting to local support points and organisations.

With the current cost-of-living crisis, ensuring that people access cash instead of debt is very important. In 2021, it is estimated that over 7 million people missed out on over £15bn of unclaimed benefits[1].

Manu Peleteiro, founder and CEO of Inbest explains that on average people using the tool have been able to access £5,000 unclaimed benefits which would go a long way in helping people to face inflation.

The initiative forms part of a much wider effort by NatWest to support its retail customers, including offering approximately 0.6m financial health checks, and proactively contacting 8m customers with support and information on the cost of living so far in 2022.

This collaboration was enabled by cluster management organisation, FinTech Scotland, which thrives to connect innovating fintech firms with established financial institutions.

The 3-month pilot of the calculator is being monitored closely before a wider roll-out to ensure customers are getting the best outcomes.

Peleteiro said:

“Benefits have powerful features to help people increase their income, reduce their expenses, and save for their future. Making sure that people are getting all the benefits they are eligible for is a great first step in a money management plan for the cost-of-living crisis. We’re looking forward to working with NatWest and helping their customers find and manage their benefits directly from the NatWest ecosystem.”

Kristen Bennie, Director of Innovation & Partnerships at NatWest Group, said:

“Making Inbest’s innovative benefits calculator available to our customers provides a critical avenue of support against the backdrop of increased cost of living pressures. Collaborating with Inbest on this pilot allows us to provide relevant, tailored and personalised insights, so we can provide support where and when our customers need it most.”

Nicola Anderson, CEO at fintech Scotland declared:

“The partnership between Inbest and NatWest is a powerful example of the purposeful impact that can be achieved through intentional collaboration between large organisations and fintech innovators. We’re proud to see this in action. NatWest has been deliberate in its focus to find new options and solutions for customers at a time of increased cost of living pressures. I know the capabilities at Inbest will make a positive difference for NatWest customers and look forward to the outcomes.”

[1] Charity Turn2Us

The role of fintech in fighting the cost-of-living crisis

Season 2, episode 3

Listen to the full episode here.

According to the Office for National Statistics, 87% of adults in the UK reported an increase in their cost of living in April 2022.

The Office for Budget Responsibility expects household incomes after tax and adjusted for inflation to start falling in Q2 2022 and not recover until Q3 2024.Since Russia invaded Ukraine, economic forecasters have raised their expectations for consumer price inflation, not just in the near term but that it will be higher for longer.On 5 May, the Bank of England forecasted inflation to peak “at slightly over 10% in 2022 Q4, which would be the highest rate since 1982”.

In this podcast we ask ourselves what the financial sector can do to help people and businesses. How can collaboration between fintechs, established firms and support organisation can improve outcomes for individuals and companies

This podcast will also be an opportunity to announce the launch of the fintech innovation labs at TSB.

Participants

Sharon MacPherson – CEO at Scotcash

Jason Wilkinson Brown – Head of Partnerships & Open Banking at TSB

Iain Niblock – Head of Product at ClearScore

Together we can do so much more: introducing Finclusion 2021

In this guest blog, Victoria Roberts, director of the Fintech Delivery Panel and Insurtech Board at Tech Nation, announces plans for Finclusion 2021, a month-long focus on fintech and financial inclusion that aims to raise awareness, inspire and support innovation, and promote collaboration.

It was Helen Keller that once said: “Alone we can do so little; together we can do so much”. She didn’t say this to disparage the efforts of individuals ”“ far from it ”“ but to highlight the power and potential of people working together.

Because there is some sort of magic ”“ some intangible spark of creativity and inspiration and innovation ”“ that happens when human beings come together in pursuit of a common goal, particularly when that goal is for the greater good.

Fighting financial exclusion

In the UK, we are at the cutting edge of fintech and innovation in financial services, and yet there are still around one million people in the UK who find themselves financially excluded.

A global pandemic hasn’t helped. While on one hand the economic and social disruption of Covid-19 has increased fintech adoption and customer use of digital propositions, it has also magnified pre-existing challenges of financial exclusion and vulnerability across society ”“ and at the same time created new ones. These include financial and personal vulnerabilities, access to services and information on financial products, intersecting struggles between health and care challenges and income instability, access to a safety net’ of affordable credit and insurance products, and the impact of lower financial literacy and planning which is often particularly highlighted in times of crisis.

Fintech as a force for good

Those of us who work in fintech can see the potential power of technology to make a real and lasting difference in this area. As we look to help individuals throughout the recovery, there is an opportunity for fintech to play a significant role in helping both those adversely impacted by recent events, and those who have traditionally been underserved by the existing financial system.

The Kalifa review highlighted the need for low cost, far-reaching fintech solutions to reach the financially excluded. Whether it is digital IDs to combat fraud, financial wellbeing apps to support sustainable financial behaviour, or a potential game-changing technological innovation that is as yet only a glimmer of an idea in the mind of a forward-thinking individual, we know from our work with fintech entrepreneurs and in helping to scale fintech companies that the talent, ideas and drive are out there ”“ we just need to support and scale it to create the change we want to see.

“Financial Inclusion is a significant driving force and motivator for so many of the fintech SME’s working in Scotland. They are working to create a more inclusive financial sector for all. Finclusion 2021 helps us highlight fintech’s power to address important social and economic challenges, and improve financial well-being for people across Scotland and the UK. We are hugely excited to be part of the Finclusion 2021 campaign, and to do what we can to encourage the whole ecosystem, from investors, founders, institutions and advisors, to embrace this opportunity to design an inclusive future of finance.

“As the Kalifa Review made clear, there is a pressing need for the undoubted ingenuity and disruptive power of fintech to be energetically applied to eradicating the obstacles to financial resilience impacting the everyday lives of our fellow citizens in the UK. This was a big problem pre-Covid: it is, arguably, nothing short of an emergency today.”

Shan M. Millie, founder of Bright Blue Hare, member of Tech Nation’s Insurtech Board, and co-chair Finclusion 2021

Introducing Finclusion 2021

That’s why we’ve launched Finclusion 2021, a series of connected happenings designed to stimulate, inspire, showcase and scale fintech’s contribution to financial inclusion, from potential game-changing products and collaborations, to the here-and-now actions being driven by the UK’s leading firms reshaping financial services.

Throughout November 2021, there will be virtual and in-person workshops, show-and-tell-events, and sprint challenges, together with thought leadership and discussion across social and traditional media.

We hope that the month-long focus will promote conversation about the key issues, inspire innovation for financial inclusion and wellbeing, and kick-start a broader call-to-action for the entire fintech community to collaborate to directly solve financial inclusion challenges to the benefit of end consumers.

“The impact of financial exclusion on peoples’ lives can be devastating, leaving many without savings or insurance, and sometimes even without access to a bank account, often having to turn to unaffordable, unregulated credit when they have no other options. If we can turn the energy and innovative ideas of the fintech community towards the development of products and services that meet people’s needs, we could help build resilience and improve financial well-being for millions.”

Chris Pond, chair of the Financial Inclusion Commission, member of Tech Nation’s Fintech Delivery Panel, and co-chair of Finclusion 2021

No one left behind

Fintech is driving fantastic innovation in financial services but, as this digitisation continues apace, we need to ensure no one is left behind. It’s great to see the fintech industry already stepping up to this challenge, and I have been inspired to see fintech firms and financial institutions coming together to listen and learn from lived experience experts during development of the campaign.

I’m really excited to see what more Finclusion 2021 can do to help educate the sector on which challenges are most pressing, and encourage innovative action to address these.

We hope as many people as possible will join us online for the virtual launch of the campaign on 3 November, where we will be sharing more information on our vision, mission and the programme of events.

We’re also inviting fintech entrepreneurs and ecosystem stakeholders to get involved by organising an event, joining the conversation, showcasing existing fintech solutions and registering to attend Finclusion events. More information on the campaign is available on our website.

#FinclusionUK2021 ”“ what part will you play?

The power of FinTech responding to the world’s worst humanitarian crises

Photo: Nur Jahan* and her daughter Ismat* (names changed to protect identity) live in the world’s largest refugee camp near Cox’s Bazar, Bangladesh. DEC funds have helped provide them and thousands of other Rohingya refugees with handwashing facilities and advice on how to stay safe from Covid-19. – Credit: Fabeha Monir/Oxfam

Article written by Huw Owen, External Relations Manager, Scotland for DEC – Disasters Emergency Committee

———————————————————————————————————————————-

When large-scale disasters hit countries without the capacity to respond, the DEC brings together 14 leading UK aid charities to raise funds quickly and efficiently.

In these times of crisis, people in life-and-death situations need our help and our mission is to save, protect and rebuild lives through effective humanitarian response.

Pooling our resources to work as one, we are pivotal in co-ordinating the UK public’s response to overseas disasters. In collaboration with our Rapid Response Network of national media and corporate partners, we raise the alarm to the UK public and set up easy ways to donate.

And we have immediate impact, getting aid to people who need it, fast.

Our current Coronavirus Appeal is funding work in eight countries – Afghanistan, Bangladesh, DR Congo, India, Somalia, South Sudan, Syria and Yemen. This includes six of the world’s most fragile states, the Rohingya refugee camps in Bangladesh, and India, which was hit by the worst outbreak of Covid-19 yet seen during the pandemic in April and May 2021.

Millions of people living in fragile states have little access to medical care or clean water, making them much more vulnerable to new, more contagious variants of coronavirus.

But in many countries the economic effects of the pandemic could be even more deadly than the virus itself as millions of people are pushed towards famine due to falling incomes and rising food prices. Hunger can be particularly devastating for children, leading to malnutrition which in the worst cases can be fatal.

The DEC is focused on

- supporting fragile health systems with PPE, equipment, and isolation and medical care facilities

- helping to give vulnerable families the means to protect themselves with water, soap, handwashing stations and information

- ensuring that the Covid-19 crisis doesn’t mean people go hungry and children become malnourished.

The UK banking and FinTech sector has had a big impact on the success of this appeal. There are several actions that corporate partners can take in support of DEC Appeals, but probably the most powerful by far is a combination of what we call “Amplify” – getting the word out to customers, clients and the public at large; and “Experience” – creating innovative new donation channels for the appeal. This combination of Amplify X Experience has delivered incredible results by raising millions of pounds in vital humanitarian aid for the people who need it most. Here are some examples of successful partnerships in this space:

The NatWest Group introduced a notification within its banking apps, prompting users to donate to the DEC Coronavirus Appeal, with incredible results.

The notification was live between October 2020 and January 2021 in the NatWest and Royal Bank apps, and raised an incredible £356,000 for the appeal. It went live again when the DEC extended its appeal to include India as a devastating surge of coronavirus overwhelmed the country, raising an additional £225,421 for India over three months.

Revolut also featured the DEC Appeal in their app ”“ Revolut has a dedicated Donations section, where over 30,000 Revolut customers have donated £262,000 to the DEC Coronavirus Appeal for India.

The DEC’s collaboration with PayPal Giving Fund has helped raise millions of pounds to benefit our appeals: in the 2019 DEC Cyclone Idai Appeal an incredible £1,320,000 was raised for emergency response, as strong winds and widespread flooding ripped apart roads, bridges, houses, schools, and health facilities and submerged vast swathes of agricultural land. Across Mozambique, Malawi and Zimbabwe, at least 900 people were killed and around three million were left in desperate need of humanitarian assistance.

PayPal amplify DEC appeals by sending email communication out to all opted-in PayPal customers at appeal launch. PayPal helps improve supporter experience by creating dedicated fundraising pages and using their “Give at Checkout” initiative. With this simple yet incredibly effective action, almost £1,000,000 was raised to benefit the DEC Coronavirus Appeal.

You can help us to build on these partnerships, harnessing the significant outpouring of concern and generosity that the UK public shows in the face of the world’s worst humanitarian crises.

Get in touch with the team at partnerships@dec.org.uk, we’d love to hear from you and explore how your FinTech can be a part of the UK’s life-saving response to international disasters.

How fintechs are driving financial inclusion

In this guest blog, Magdalena Krön, Rise Global FinTech Platform Director, Barclays Ventures, takes a look some of the work that the global fintech community is doing to address one of the biggest blights in society ”“ financial exclusion. This blog is based on the latest Rise FinTech Insights, a regular publication from Rise, created by Barclays.

One thing that COVID-19 teaches us, if we needed reminding, is how many people across the world remain disadvantaged by not having access to basic financial services. Although efforts to improve financial inclusion have come a long way in a relatively short period of time, there is still much more to achieve, especially for the 1.7 billion individuals who are currently unbanked(1). The work being done in the fintech space to address this issue, intended to open doors for individuals and families in a way that many of us take for granted, has seen entrepreneurs deploy everything from cryptocurrency to Open Banking and APIs in efforts to find new ways to support the financially vulnerable.

Chris Britt, Co-Founder and CEO of Chime ”“ a leader in the US challenger banking segment that offers internet-based, fee-free services ”“ says, “There is a huge segment of America that has a lot of anxiety around their money and day-to-day finances.” Helping them achieve “financial peace of mind”, he says, starts with providing a banking relationship that doesn’t rely on fees. “As many as 70% of Americans live paycheck to paycheck ”“ we offer free services such as early access to paychecks and overdraft protection.”

Innovative fintech thinking has come to the aid of another swathe of US society: the 2.5 million newcomers to the country on long-term visas who are, for the most part, unable to access credit. Collin Galster, Head of Business Development at Nova Credit, identified a solution to this problem facing the US’s foreign-born population, which is set to rise to 50 million by 2030. The company, a cross-border credit bureau, transfers individuals’ financial histories from one country to another, remedying the issue of lenders not being able to access enough financial information to feel comfortable lending, and therefore enabling immigrants to start funding their futures.

The need to tackle financial exclusion is felt even more acutely elsewhere. In India, for example, almost 11% of the adult population is unbanked. The report highlights a number of successful government initiatives, including Jan Dhan Yojana and Aadhaar Pay, that are spearheading more accessible paperless Know Your Customer (KYC) identification processes and biometric-based identity payment systems. This is a tactic that saw the number of people holding bank accounts increase by just over 50% between 2014 and 2017. Manish Khera, Founder and CEO of HAPPY ”“ a digital lending app targeting a multi-billion-dollar credit gap in India’s micro businesses ”“ emphasises how the internet now plays a vital role in facilitating and widening this access, citing the fact that India currently has 520 million mobile internet users.

Alternative banking solutions are springing up elsewhere, too. In east Africa, for example, Anisha Kothapa, Fintech Analyst at CB Insights, says cryptocurrency is being “adopted widely” ”“ offering a new way for the unbanked to save money and complete transactions without needing an account or credit card. One firm leading the way is Kenya’s BitPesa, a digital currency payments platform that “allows users to accept bitcoin payments, exchange bitcoin for local currency, and deposit bitcoin into accounts or mobile money wallets.”

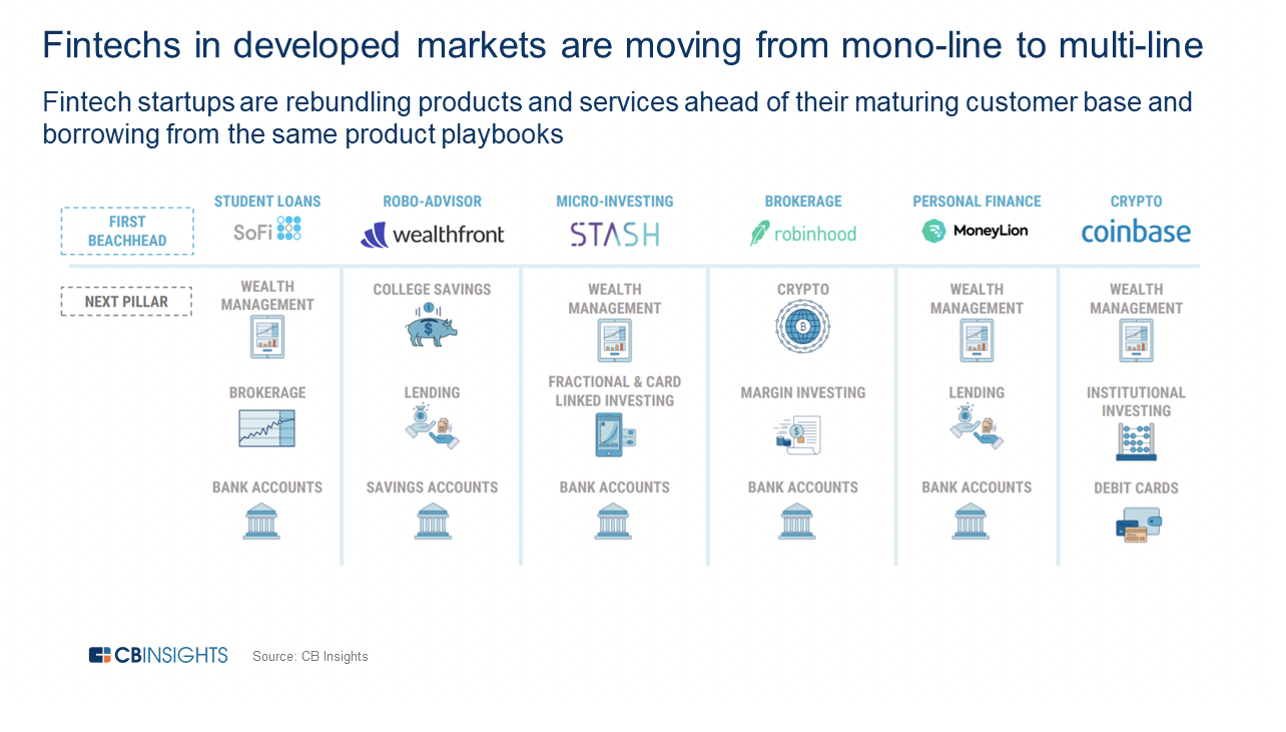

In contrast to developing countries, their developed counterparts are enabling financial inclusion differently by focusing on customer engagement and transforming the entire banking business model. FinTechs in developed markets are also moving from mono-line to multi-line offerings and re-bundling products and services to acquire more new customers.

It’s not just individuals that face financial exclusion, the report emphasises, but SMEs and budding entrepreneurs. According to Grant Bickwit, Associate at Barclays International, access to capital is one of the biggest challenges faced by entrepreneurs. It’s a sad truth, he explains, “that both entrepreneurs and investors are still reliant on individual networks and legacy processes for sourcing opportunities, entrenching geographic and social limitations”. In response to this, online platforms like OnDeck and Kabbage, launched in 2006 and 2009 respectively, offered firms access to credit digitally ”“ a trend that has proliferated.

Rise innovators have been responding to some of the other unique issues brought about by the pandemic, from employment to supply chain management. Rise Mumbai members, MMS.IND and GeoSpoc ”“ experts in geospatial information systems, platform-building, and consumer and micro-market data ”“ have joined forces to develop a COVID-19 impact tool which provides insights into how the pandemic is affecting consumers ”“ and enables businesses to better predict demand and ensure supply chain optimisation. Meanwhile, over at Rise New York, Brainceek, a workforce simulation company, has been helping corporates design virtual summer internship curriculums, providing extra support for the hundreds of thousands of graduates entering a difficult job market.

Addressing financial exclusion is a huge task, but one that is achievable, particularly with targeted collaboration across banks, technology companies and fintechs and a focus on achieving financial inclusion for those 1.7 billion individuals.

Download all editions of Rise FinTech Insights here.

(1) https://www.worldbank.org/en/topic/financialinclusion/overview

How a fintech is helping people to receive affordable loans

The University of Edinburgh and Scottish fintech Inbest are collaborating on a research project that aims to address the challenge of accessing income benefits and affordable finance swiftly for those individuals who have suddenly been made financially vulnerable as a result of the current COVID-19 pandemic. The project has been awarded a Data-Driven Innovation Grant Innovation and also has the support of Scotcash and Advice Direct Scotland.

The project will propose a new credit assessment method that takes into account the amount of benefits that the applicant is entitled to receive and will suggest a repayment schedule based on the applicant’s timeframe of receiving the benefits and their expense behaviour. This method will help affordable lenders to make better short-term lending decisions for individuals who otherwise may fail to meet the standard credit risk models. The project will leverage on Inbest Benefits calculator and its banking analytics platform to calculate individuals’ benefits entitlement and financial situation.

The project came to light as a response to the priorities underlined by the Scottish Fintech Consumer Panel – an industry group set up by Fintech Scotland that aims to support inclusive fintech business development by connecting citizen advocate groups into the fintech ecosystem. The consumer panel played a fundamental part in the project proposal by defining the project scope and connecting the participants.

Raffaella Calabrese, Associate Professor at University of Edinburgh Business School, said:

“We are delighted to work on such a pressing issue for Scottish citizens as, in the last month, Scotland has seen 130,000 new applications for Universal Credit, compared with 20,000 the same time last year. Our objective is helping financially vulnerable customers to access cheaper sources of financing and improve their resilience to financial shocks. Customers’ credit capacity will be further enhanced as the lending assessment will also include the potential impact of financial recommendations such as their benefits entitlement”.

Manu Peleteiro, CEO of Inbest, said:

“This project is another great example of how Scottish institutions and companies are collaborating to develop data-driven solutions to improve financial inclusion. We are looking forward to sharing the lessons learned from this project on the Fintech Consumer Panel, raise awareness of financial vulnerability and drive new initiatives to improve design access and management of benefits and affordable loans”.

Nicola Anderson, Strategic Development Director at FinTech Scotland welcomed the initiative.

“This initiative demonstrates the real value of bringing citizen and consumer needs to the forefront of FinTech development. Using focused research and data analytics, the collaboration between Inbest, the consumer groups and the University of Edinburgh’s has helped develop an enterprise that can help people at a time of crisis and real need. It’s another great example of how inclusive innovation in financial services can deliver good outcomes for people and society”.