The Future of Financial Advice: Consumer Expectations for 2025 and Beyond

The Financial Advice Consumer Survey 2025, conducted by Scottish fintech Aveni in collaboration with YouGov, highlights key trends shaping the future of financial advice in the UK.

With rising concerns about financial security, regulatory demands for enhanced consumer protection, and the increasing role of artificial intelligence (AI) in financial services, this report highlights the areas where financial firms must innovate to stay ahead.

There full survey can be found here.

Key Findings from the Survey

Consumers Demand More Personalised and Accessible Advice

A growing number of consumers expect financial advice to be tailored to their specific needs rather than generic recommendations. According to the survey, many individuals feel underserved by traditional financial advisory models and are looking for more dynamic, AI-driven solutions that provide real-time insights.

Trust in Financial Advice is at a Crossroads

Trust remains a critical issue in financial services. While robo-advisors and digital platforms are gaining traction, many consumers still prefer human interaction for major financial decisions. (42% of respondents expressed concerns about receiving financial advice solely from AI-powered tools).

AI and Automation are Reshaping Financial Advice

AI is playing a larger role in financial planning, from analysing spending habits to recommending investment strategies. However, consumers have mixed feelings about relying solely on AI-driven solutions.

Regulation and Consumer Protection are Driving Change

As regulatory bodies push for greater consumer protection, financial firms must adapt to new compliance standards. The Consumer Duty Act, for example, is set to reshape how firms engage with customers, ensuring fairer outcomes and more transparent advice. (72% of respondents stated they want clearer explanations of financial products and risks).

Rising Financial Anxiety and the Need for Proactive Guidance

Economic uncertainty, inflation, and concerns about long-term financial stability are leading consumers to seek proactivefinancial guidance rather than reactive advice.

What Does This Mean for Financial Firms?

The findings highlight several key takeaways for financial firms and advisors:

- Embrace AI-powered financial tools while maintaining a human-centric approach.

- Increase transparency around fees, data usage, and product recommendations.

- Develop digital-first advisory models that cater to on-demand financial guidance.

- Improve consumer education to enhance engagement and financial confidence.

- Stay ahead of regulation by prioritising customer outcomes and compliance.

Read the full report here.

Consumer Duty and Beyond

Season 5, episode 2

Listen to the full episode here.

In this episode, we explore the complex challenges and opportunities that organisations face in delivering greater transparency, fairness, and accountability.

As the industry evolves, both fintechs and established financial institutions must navigate these demands to not only meet regulatory requirements but also to exceed them through innovation, ethical practices, and customer-centric strategies.

With Sajedah Karim – Partner at PwC. Sajedah

Joseph Twigg – CEO at Scottish fintech Aveni

John Finch – Professor of Marketing (B2B) at the University of Glasgow’s Adam Smith Business School, and Associate Dean (East Asia) at the University of Glasgow’s College of Social Sciences.

Hope4u: Empowering People Through Financial Innovation

Throughout their lives, people will more often than not face financial challenges at some point. Recognising this, Hope4u, a fintech part of the FinTech Scotland community, is transforming how families navigate these hurdles with its innovative digital solutions.

What is Hope4u?

Hope4u is a fintech platform designed to provide tailored financial support for people in difficult financial situations. By leveraging advanced data analytics and user-centric design, Hope4u enables individuals and families to access grants, manage their budgets, and find relevant support services—all in one easy-to-use app.

How Hope4u Works

The platform connects users with financial assistance programs and resources in their region, helping them make informed choices about their finances.

• Personalised Financial Assistance Finder: Using intelligent algorithms, Hope4u matches families with benefits, grants, and services that align with their specific needs and eligibility criteria.

• Budgeting Tools: people can set financial goals, track expenses, and receive tips on managing household budgets effectively.

• Access to Community Resources: Hope4u links users with local support networks, childcare providers, and education resources, creating a holistic support system.

Making a Broader Impact

By addressing challenges like financial inclusion and resource accessibility, Hope4u is helping individuals across the UK thrive in uncertain times.

For example, Hope4u enables users to discover and apply for financial aid programs similar to Scotland’s Scottish Child Payment or Best Start Grant, demonstrating its adaptability to regional contexts. The platform’s flexibility ensures it can support families regardless of their location, making it an invaluable tool for those navigating complex financial landscapes.

Lloyds Banking Group Partners with Scottish FinTech Inbest to Launch New Benefits Calculator

Lloyds Banking Group has partnered with Scottish fintech Inbest to launch a new tool aimed at helping millions of UK households access unclaimed benefits. The benefits calculator, now available in the Lloyds mobile banking app, is designed to bridge the gap between people and the £23 billion of unclaimed benefits such as Universal Credit and council tax support.

How It Works

The calculator is simple and intuitive. Users start by answering six quick questions about their household, income, and living situation. Based on this initial input, the tool provides an estimate of potential benefits they might be entitled to. For a more detailed analysis, users can complete a five-minute questionnaire to receive a final summary of their benefits eligibility.

If eligible, the calculator doesn’t just stop at telling users what they might claim; it also provides direct links to begin the application process. Additionally, the tool highlights potential grants for home improvements or energy efficiency upgrades.

Tackling a National Problem

Lloyds Banking Group’s initiative is a direct response to the estimated eight million UK households missing out on financial support. With the cost-of-living crisis intensifying, the “More Money in Your Pocket” hub in the Lloyds app aims to provide tangible assistance to those who need it most.

Since its soft launch, the benefits calculator has already helped thousands of users identify new sources of financial support. The tool is available on both iOS and Android devices, ensuring broad accessibility for Lloyds customers.

A Collaboration for Impact

This innovative solution was developed in partnership with Inbest, a leading Scottish fintech specialising in financial inclusion technology. Inbest’s expertise in building user-friendly tools to simplify financial complexity was instrumental in creating the benefits calculator.

FinTech Scotland, which supports collaborations like this, continues to highlight the power of partnerships between established financial institutions and fintech innovators. By joining forces, Lloyds Banking Group and Inbest are leveraging technology to deliver impactful financial solutions for everyday consumers.

“We’ve launched Benefit Calculator, helping customers to identify the benefits they may be eligible for and providing clear guidance on making a claim.”

This partnership with Inbest is a testament to the growing importance of fintech collaborations in addressing societal challenges. By combining Lloyds’ reach and resources with Inbest’s innovative capabilities, this initiative marks a significant step towards greater financial inclusion across the UK.

Good tech is the answer to the vulnerable customer challenge

In February 2021, the Financial Conduct Authority (FCA) introduced comprehensive guidance aimed at ‘ensuring the fair treatment of customers in vulnerable circumstances. This was driven by the recognition that vulnerable people, because of circumstances such as poor health, financial instability, or negative life events, are particularly susceptible to harm if not “treated fairly”. The FCA’s guidance outlines actions firms should take to understand and address the needs of these customers, ensuring they receive “outcomes which are as good as other customers’”. The goal is to create a financial services environment where all customers, regardless of their circumstances, are treated fairly and with respect.

This requires firms to:

- Understand everyone’s characteristics and to mitigate any potential harms.

- Monitor the consumer through the lifetime of the product/service.

- Report on outcomes of vulnerable cohorts, compared to the resilient, for Consumer Duty reporting.

- Assess and report on the fair value received by vulnerable cohorts, compared to the resilient.

- Maintain evidence of the above.

None of this is easy. The first challenge is how to identify those customers who are vulnerable. Firms are attempting to do this in several ways, dividing them into indirect, or reactive, methods – essentially assessing current data sources – and direct, or proactive, methods – engaging directly with the consumer.

While it’s true that there is a lot of financial data available which can infer financial vulnerability, this is only part of the picture – there is minimal information available on health and lifestyle. Focusing on only financial data provides a woefully incomplete picture. Indirect approaches are largely limited to financial characteristics; the only practical way to obtain health and lifestyle information is to engage directly with consumers. This is very successful. Firms can obtain good information, directly from consumers, using voice analytics, face-to-face meetings or calls, voice calls, questionnaires and similar approaches.

AI is heralded as a silver bullet – but in the absence of a library of vulnerability data on which to train the AI model, this is currently little more than wishful thinking.

We know that around 50% of people are vulnerable at any one time. The only way to identify that 50% is to assess everyone. Far too many firms began by using reactive methods – waiting for customers to inform them of their vulnerabilities or waiting for vulnerabilities to be identified at points of interaction. These approaches are seldom adequate – identifying few people – so most firms are looking to be both more proactive and thorough in their assessment methodologies.

Once we identify vulnerabilities, the next challenge is how to classify and store the data – with around 100 characteristic data points, each having a range of severities, there is a lot of data on which to base an assessment. If undertaken manually, understanding (and therefore assessment) is subjective – and many early approaches used text descriptions. These are inconsistent and difficult (if not impossible) to use structurally for assessment, management and reporting. Proprietary lexicons of vulnerability bring an objective assessment methodology which delivers consistent data. One such system is the MorganAsh Resilience System (MARS).

After identification and classification, there is the thorny challenge of GDPR. We need to restrict data to only those who need it, while communicating vulnerabilities across firms so that mitigation strategies can be used. Many firms have yet to resolve this. The solution is to code, classify and communicate characteristics – and mitigating strategies – so that an individual’s personal data is not openly passed around.

The next challenge is how to mitigate customers’ vulnerabilities. Many solutions are obvious, and, with flexibility, these can be implemented by front-line staff. However, this approach is too limited to be successful. There is a vast number of mitigations strategies that might be appropriate, vast numbers of consumer groups to signpost to – and firms may have different appetites for customer service for different groups. It’s unrealistic to expect busy staff to be experts in all vulnerabilities and mitigation paths. Again, systems are required to deliver consistency and scalability.

A further development is how vulnerability data is shared between firms. In an intermediated market – which is most of the financial services industry – manufacturers’ products are sold via intermediaries. Typically, intermediaries have contact and relationships with consumers, while the manufacturer maintains the product – often over multiple years. To meet the monitoring obligation, either the intermediary and the manufacturer undertake separate vulnerability assessments, or they collaborate and share information. The industry has been slow on this, with minimal discussions between groups.

While customer vulnerability is a very human issue, for it to be managed it needs data – and systems to support this data. The good news is that this is already happening. Vulnerability tech systems are already in place and working well – and pioneering the new discipline of vulnerability management.

Want to read the full report? Visit https://www.elephantsdontforget.com/resources/customer-vulnerability-your-questions-answered-2/

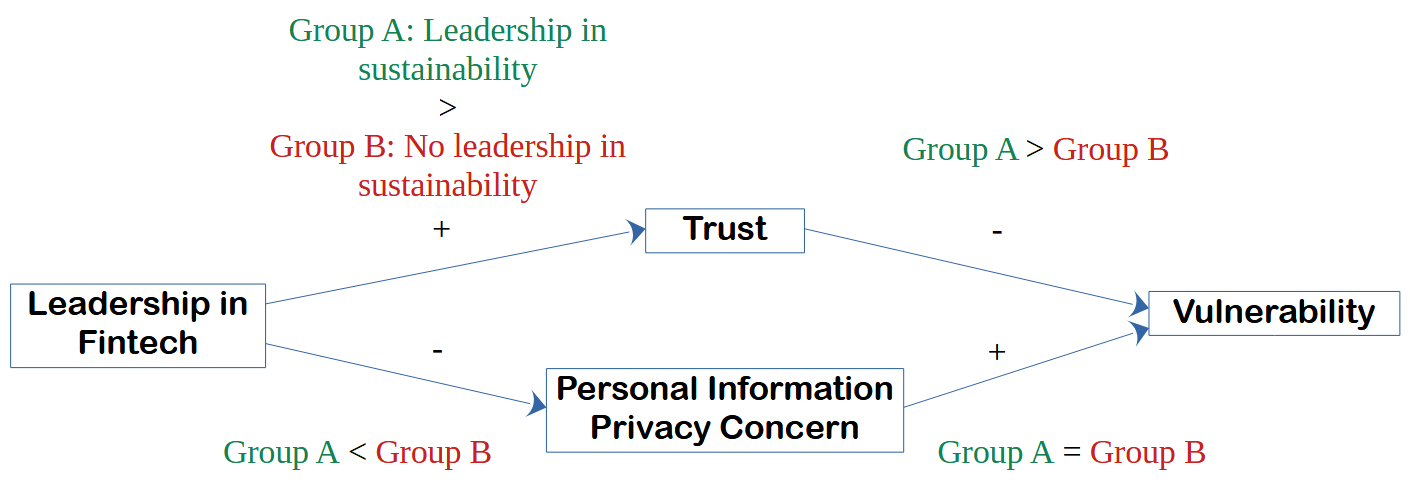

Leadership in Fintech builds trust and reduces vulnerability

Article written by Dr Alex Zarifis

Fintech and sustainability

Financial technology often referred to as Fintech, and sustainability are two of the biggest influences transforming many organisations. However, not all organisations move forward on both with the same enthusiasm. It is, therefore, important to find the synergies between Fintech and sustainability. For this reason I carried out research on how leadership in Fintech builds trust and reduces vulnerability when combined with leadership in sustainability (Zarifis, 2024).

Leadership in Fintech and sustainability

One important aspect of this transformation many organisations are going through is the consumersʹ perspective. It is important to clarify whether leadership in Fintech, with leadership in sustainability, is more beneficial than leadership in Fintech on its own.

This research evaluates consumers”™ trust, privacy concerns, and vulnerability in the two scenarios separately and then compares them. Firstly, this research seeks to validate whether leadership in Fintech influences trust in Fintech, concerns about the privacy of personal information when using Fintech, and the feeling of vulnerability when using Fintech. It then compares trust, privacy concerns and vulnerability in two scenarios, one with leadership in both Fintech and sustainability, and one with leadership just in Fintech without sustainability.

The benefits of combining leadership in both Fintech and sustainability

The findings show that, as expected, leadership in both Fintech and sustainability builds trust more, which in turn reduces vulnerability more. Privacy concerns are lower when sustainability leadership and Fintech leadership come together; however, their combined impact was not found to be statistically significant. So contrary to what was expected, privacy concerns are not reduced more effectively when there is leadership in both together.

Figure 1: Model of leadership in Fintech, trust, privacy and vulnerability, with and without sustainability

Fintechs can use these findings to make consumers feel less vulnerable

An important practical implication is that this research finds that even when there is sufficient trust to adopt and use Fintech, the consumer often still feels a sense of vulnerability. This means leaders in Fintech must not just do enough for the consumer to adopt their service, but they should build trust and reduce privacy concerns enough for consumers to feel less vulnerable. These findings can inform a Fintech”™s business model and the services it offers.

Reference

Zarifis A. (2024) Leadership in Fintech builds trust and reduces vulnerability more when combined with leadership in sustainability”™, Sustainability, 16, 5757, pp.1-13. https://doi.org/10.3390/su16135757

Biography

Dr Alex Zarifis research and teaching are on the practical applications of technology in business. Before the University of Southampton, he worked at several academic institutions including the University of Cambridge and the University of Manchester. He is currently a research affiliate of the Cambridge Center for Alternative Finance (CCAF).

His research interests include trust, electronic business, artificial intelligence, blockchain, Fintech and Insurtech. He has over forty publications and his work has featured in journals such as Computers in Human Behaviour and Internet Research. He has explored cryptoassets such as cryptocurrencies since 2012. As part of this research, he published the first peer reviewed research on trust in digital currencies in the world in 2014.

Banking on Everyone

In an era where digital technologies shape our daily lives, financial inclusion remains a pressing issue worldwide. Many individuals and communities still face barriers to accessing basic financial services. However, amidst these challenges, Financial Technology (Fintech) is emerging as a transformative force, bridging the inclusion gap and bringing banking services to everyone, regardless of their background or location.

The Rise of Fintech

Fintech refers to the innovative use of technology to deliver financial services. In recent years, Fintech has gained momentum globally, disrupting traditional banking models and democratising access to finance. Scotland, with its vibrant tech ecosystem, has been at the forefront of this revolution. From mobile banking apps to peer-to-peer lending platforms, Fintech startups are reshaping the financial landscape, making it more inclusive and accessible to all.

Empowering the Unbanked

One of the most significant contributions of Fintech is its ability to reach the unbanked and underbanked populations. In Scotland, as in many parts of the world, there are individuals who have limited or no access to traditional banking services due to factors such as geographic remoteness, unemployment, disability or lack of documentation. Fintech companies are addressing this challenge by offering digital banking solutions that can be accessed through smartphones, eliminating the need for physical bank branches and paperwork.

Innovative Solutions for Financial Access

Fintech innovation goes beyond traditional banking services, offering a wide range of solutions to enhance financial access and inclusion. For example, microfinance platforms leverage technology to provide small loans to entrepreneurs and individuals who lack collateral or credit history. Similarly, blockchain-based payment systems enable cross-border remittances at lower costs, benefiting immigrant communities and their families back home. These innovations are not only expanding financial access but also promoting economic empowerment and social inclusion.

Challenges and Opportunities

While Fintech holds immense potential for promoting financial inclusion, it also faces challenges such as digital literacy, cybersecurity, and regulatory compliance. Moreover, there is a risk of widening the digital divide if segments of the population are not included in the transition to digital finance. To drive financial inclusion collaboration between Fintech firms, government agencies, and civil society is essential. By working together, stakeholders can develop policies and programs that promote inclusive Fintech solutions and ensure that no one is left behind in the digital economy.

In Scotland and beyond, Fintechs play a pivotal role in bridging the inclusion gap and creating a more equitable financial system. By leveraging technology and innovation, Fintech firms work towards empowering individuals and communities to access essential banking services, build assets, and improve their livelihoods. The unbanked are the people who hold the key, organisations willing to go the extra mile to attract, employ and work in partnership with individuals to understand their challenges and fears will be the organisations that cross that finish line first. Occasional focus groups and questionnaires are not enough, building strong robust and trusting communities is the only way to solve challenges.

As we continue to embrace the digital age, can we harness the power of Fintech to build a more inclusive and prosperous future for all? No one can be left behind.

About the Author

Laura Bosworth has worked in the recruitment and employer branding industry for many years. Based in Scotland and working with clients across a range of sectors and industries in the UK and the US.

A diversity, equity and inclusion leader she aims to unlock economic opportunity for all

because everyone deserves a fair chance. Over the course of her career, she has had the privilege of building and executing hiring strategies and programmes that help level the playing field and create employment pathways into Technology, Professional Services and Financial Services.

Laura consults with senior executives at FTSE 250 and Fortune 500 companies on developing diverse recruiting strategies backed with insights, including empowering and connecting emerging and established minority leaders across the globe. Motivated by the ability to have a social impact at scale, building empowered teams and influencing leaders to make more inclusive and intentional decisions.

Photo by Andrew Neel: https://www.pexels.com/photo/apple-iphone-desk-laptop-6633921/

Revolutionising Financial Futures: UK Fintech Challenge Pioneers Data-Driven Solutions for Later Life Planning

FinTech Scotland and Smart Data Foundry are collaborating to bring an industry-wide UK fintech innovation challenge to the market. This challenge seeks to inspire the development of inclusive financial services for consumers, empowering them on their journey towards a secure financial future.

Building on the success of the previous SME business banking programme in 2023, the 2024 emphasis will be on new innovative solutions that can support people’s financial journeys as they plan for their later years.

UK fintechs can now apply to take part in the challenge, and up to six successful applicants will be awarded a £5K participation fund to allocate resource to developing their idea. In addition to funding, the challenge offers a fantastic opportunity for participants to present to some of the largest financial institutions in the UK, including NatWest Group, PwC, and Royal London, as well as engage with experts in data, technology, and fintech. This exposure will allow innovators to gain valuable insights, receive expert guidance, and enter potential collaborations, maximising the chances of success for their projects.

Another key feature of the challenge is Smart Data Foundry’s provision of synthetic data replicating both consumer banking and investment and savings products*. This will enable fintechs to thoroughly test and refine their innovations, ensuring the development of robust and effective solutions that address consumers’ real needs.

As life expectancy in the UK and around the world continues to increase, the number of people living later in life is growing rapidly. It is expected that average life expectancy in the UK will be 85.9 years by 2050 – in 1950 it was 68.6 years.1 This demographic shift has a significant impact on the current and future cost of living, as there is an increased need to be financially secure for longer. Fintech solutions need to consider future products and services that will help prepare people financially for a longer life.

Through support from the Strength in Places UK Research and Innovation Grant, a prize fund of £45K will be offered to promising projects arising from the challenge. This will allow entrepreneurs and innovators to further develop and implement their ideas, which will help unlock later-life planning for consumers.

Those interested in taking part have until 17 May to submit their application.

Samantha Brand, Innovations & Partnerships at NatWest Group, said:

“We are thrilled to partner with FinTech Scotland and Smart Data Foundry on the innovation call for Supporting Later Financial Lives. This growing customer segment spans life stages with varying product requirements, and we believe there are specific needs to be solved in this space. We look forward to working with innovators to understand how we can create the best solution for our customers. The challenge aligns firmly with NatWest’s purpose to champion potential, helping people, families and businesses to thrive.”

Sarah Collins, Director PwC United Kingdom, commented:

“We are thrilled to support this innovation challenge, which represents an exciting opportunity to harness the power of open finance data. The power of fintech can help consumers gain greater control over their financial futures, ultimately enabling them to make smarter decisions as they plan for later life. We are delighted to be working with FinTech Scotland and Smart Data Foundry to accelerate data driven innovation.”

Bryn Coulthard, Chief Product and Technology Officer at Smart Data Foundry, said:

“Our continued partnership with FinTech Scotland in this innovation challenge underscores our commitment to empowering consumers with innovative, data-driven solutions. By leveraging the power of data, technology, and fintech expertise, we hope this challenge will help to revolutionise financial services, ensuring individuals can embark on their later years with confidence and security. Through initiatives like this, we’re envisioning the future and actively shaping it.”

Nicola Anderson, CEO of FinTech Scotland, said:

“Together with Smart Data Foundry, we are excited to launch this new innovation challenge focusing on later financial lives. As we explore innovation in this domain we hope it will also generate fresh insights into the potential for Open Finance data. This is a great opportunity to explore that potential, with a focus on delivering smarter, and future-focused customer solutions. We are excited to see how these new ideas will help evolve the digital financial landscape with a focus on accessibility and using data to capture the needs of our rapidly evolving society.”

Those interested in taking part can find out more here: FinTech Scotland | Innovation Challenge to support consumers in their later financial lives.

Tesco Bank and Black Professional Scotland driving diversity and inclusion

Blog written by Fiona Allan, Senior Clubcard Proposition Manager at Tesco Bank

Through our great collaboration with Fintech Scotland, we received an introduction to Black Professionals Scotland and over time have built up a strong relationship where we have been able to grow our participation with their excellent internship programme.

As a business, we are passionate about increasing the diversity of our workforce and making sure we can support those from under-represented backgrounds. In our most recent intake, we welcomed 16 interns from Black Professional Scotland to join us for our 12-week internship program.

Tawa joined us in Oct of last year as Innovation & Loyalty intern. She hit the ground running having finished her Master’s degree at Robert Gordon’s University in Aberdeen just days before starting with us! This was the first time we had welcomed an intern to our team, and we were excited to get Tawa involved in the work we lead on proposition development and Clubcard.

When designing the intern experience, it was really important that we focused on giving our intern the most breadth in terms of their experience and visibility right across the Tesco group. Tawa’s project focus was developing Clubcard propositions, specifically looking at how we bring the best of Clubcard to our travel propositions.

During Tawa’s first couple of weeks, I set her up with induction meetings with colleagues from across the business. Having never working in Financial Services before, I was keen for her to build a solid foundation with an understanding of our products, how they worked, and our relationship with the wider Tesco group. Tawa found these initial meetings extremely valuable and continued to build these positive relationships with her stakeholders throughout her internship.

Personal development is something we’re very passionate about here at Tesco Bank, and during the 12 weeks we had together, I was keen to do everything I could to help her build a clear focus on her development. We found Tawa a mentor to help support her and offer some guidance on navigating the next steps in her career and the world of Tesco. We set three core focus areas for development and supported her to build her skills in presenting, storytelling, and stakeholder management.

Tawa was based in Aberdeen, so we agreed that she would commute to Edinburgh 1-2 days per week to get face time with the team and work remotely for the rest of the week. This time in the office was extremely valuable for Tawa to build relationships and spend time with the other interns. In addition to her time working in the Edinburgh office, Tawa also made time to attend multiple industry events, including a FinTech Scotland conference, a day spent with our Customer Service teams in Glasgow, and networking events organised by Black Professional Scotland.

Mid-way through the internship, I organised a trip down to Tesco HQ in Welwyn Garden City. Although her internship was with the Bank, I wanted Tawa to have the opportunity to see and experience as much of the wider Tesco business as possible. This trip gave Tawa the opportunity to step out of the world of finance and into the world of food, where she met colleagues working in the wider Clubcard team and even had time for a tour of the Tesco innovation hub, Tesco labs.

Having Tawa in the team for 12 weeks was hugely valuable, not only was she a pleasure to work with, but she was also a valued member of the team who brought an incredibly insightful outside perspective. She challenged and expanded our thinking, while giving a clear recommendation for her project on future Clubcard travel propositions.

It was a pleasure to watch Tawa develop and grow in confidence throughout her internship and I know she’ll go on to be a huge success in whatever she does. Tawa has now successfully secured a working Visa for the UK and is looking for permanent jobs. She knows she has allies at Tesco Bank that she can call on, and a mentor in me who will support her in any way I can.

I wouldn’t hesitate to work with Black Professionals Scotland again to welcome another intern to our team and help offer more opportunities to diversify the workforce within the FinTech industry. Thanks again to our continued strong collaboration with Fintech Scotland, being able to make these powerful connections in the industry.

Fintech – a force for good

Season 4, episode 1

Listen to the full episode here.

Episode recording with Fintech Australia.

Fintech has emerged as a transformative force in the financial sector, offering innovative solutions that not only enhance financial services but also address broader societal issues, including environmental sustainability, customer vulnerability, and overall financial well-being.

Those objectives are heavily featured in the Research & Innovation Roadmap that we published 2 years ago.

In Scotland, we have an important number of fintechs addressing those challenges. In fact, the majority of Scottish fintechs are fintech for good.

Today we’ll take some time to consider how those organisations are driving positive changes.

Guests:

Ren Hooi, Founder and CEO at Lightning Reach

Robin Peters, Co-founder and CEO at Snugg

Sheila Hogan, Founder and CEO at Biscuit Tin